Lights, camera, action!

Well... maybe not the lights part.

December has kicked off in the worst way possible for Saffers, as Eskom announced Stage 6 loadshedding to be implemented for the entire week…

...and provided a firm warning of potentially higher levels as we head to the 'festive season'! Investors have already been on the tenterhooks over the drama surrounding President Ramaphosa, which saw the Rand tumble against the greenback…

... and if last week showed us anything, it would be that all indicators suggest that the local political and economic landscapes are in for a turbulent final few weeks of 2022.

So, without further ado, here’s your weekly dose of our Rand Review!

Key Moments (5-9 Dec 2022)

Dominating the week's headlines were the following:

- “Farmgate” frustrations - President Ramaphosa was handed a lifeline after the ANC confirmed that it would request lawmakers to reject a report that claimed he may have violated the constitution.

- US Services and PPI - The world’s top economy’s service industry activity and PPI results improved in November, offering additional evidence of underlying momentum in the economy.

- Eurozone GDP - Economic growth in Q3 was confirmed at 0.3% for the Eurozone, but experts remain cautious as energy reserves continue to deplete heading into winter.

We begin our weekly quest at home…

... where the local unit was starting to recover from a calamitous collapse after the political turbulence created by recent reports relating to President Ramaphosa and the Phala Phala incident. The Rand was changing hands at around R17.30/$ in the early market session on Monday, ahead of a meeting by the executive committee of the ANC to decide the fate of the country’s President.

The end decision taken by the country’s ruling party was to back the President by agreeing to reject a document that reportedly indicated that he may have violated the constitution.

Wow!

What next...?

Perhaps the less said about this, the better...but it will come up again. The cover up only last for so long...

...nevertheless, the decision seemingly forestalled the fears of immediate political fallout, and the local unit benefited, dropping to R17.15/$ by early afternoon.

Overnight the dollar strengthened on most counterparts as markets were digesting the unexpectedly strong ISM Non-Manufacturing PMI results from the US.

The strong service industry results also came hot on the heels of a (on the surface) robust US jobs report - and in what’s become a common reaction - markets moved into “good news is bad” mode.

something which continues to keep economists befuddled...

...fact is, the markets are predictably irrational)

Speculation began to swirl over the Fed potentially needing to become more Scrooge-like and perhaps unwrapping another unwelcomed super-size rate hike at next week’s meeting to cool the economy.

As the greenback gained support, the local unit was forced to give back the gains it made and was trading in the mid R17.40s for most of Tuesday, with a few crucial local economic data releases incoming.

All of these made for positive reading!

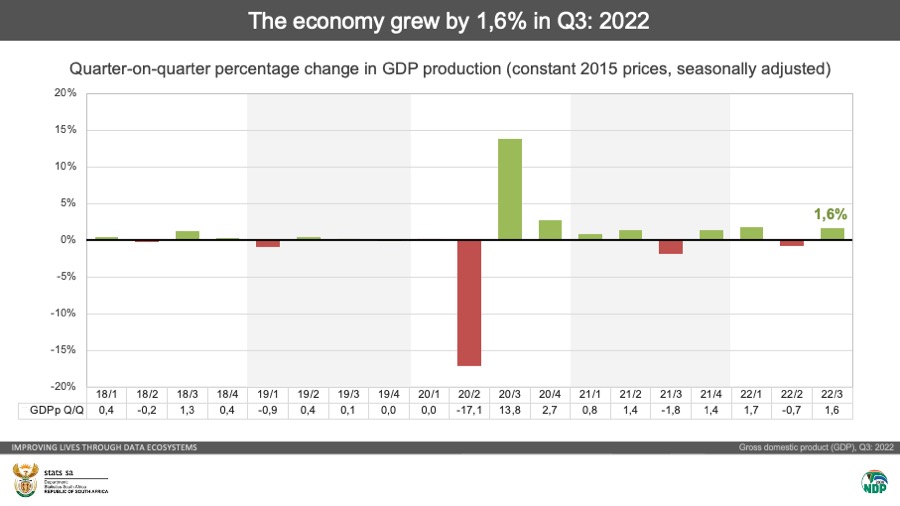

The first was the GDP results, which showed that the local economy expanded admirably, registering a 1.6% growth in Q3.

Production from agriculture, forestry, and fishing, combined with services in the finance and business sectors, contributed the lion’s share of the GDP growth.

The final piece of data released revealed that South Africa’s current account deficit reduced to 0.3% of GDP in Q3 from 1.6% in Q2.

In Rand terms, that means the deficit for Q3 was R18.1 billion, from R107 billion in Q2.

While the positive data readings helped strengthen the local unit through the middle of the week, there was one major setback that threatens to undo any further improvements in Q4'22…

...Eskom!

The country’s struggling power supplier rear-ended the economy this week with the fourth edition of Stage 6 loadshedding, as breakdowns of equipment and mismanagement continue to restrict performance.

In addition, with the prices of energy and fuel continuing to remain elevated, battered consumers are finding it increasingly difficult to pay sky-high bills, which are adding to Eskom’s financial woes. Officials have mentioned that there is a very strong possibility of higher levels of rolling blackouts in the upcoming weeks and months.

The fact is that that coffers are running dry - causing an inability to purchase diesel to support normal operation.

The scariest part of all this is:

While unthinkable, if higher levels of loadshedding are implemented, the current structure only covers up to stage 8.

In the meantime, the country’s President seems more distracted with dealing with impeachment threats, fighting factional battles within the ruling party, and signing declarations of additional public holidays than dealing with Eskom’s, and the country’s crisis.

Let’s hope it gets the attention it requires before it’s too late, that is, if it isn’t too late already. Guess we’ll have to wait until next week to find out.

Onto other news:

- The Eurozone’s Q3 economic growth was confirmed at 0.3% in the week, helping the shared currency to push back toward the €1.06/$ region. The ECB’s final meeting of the year is due to be held next week with at least a 50 basis point increase all but locked in.

- In November, inflation fell for the first time in over a year, but the current 10% level is a long way from the ECB’s 2% target range. Another growing concern for the EU is that re-stocking of gas storage in the near future could be extremely costly, especially if China is able to move toward a full reopening of its economy in 2023.

In its latest data release, Chinese exports and imports were shown to have shrunk in November at their steepest pace for over 2 years. Dwindling domestic and global demand, combined with lockdown-led production supply drops and a property slump, is weighing heavily on the world’s number two economy. Exports dropped by a massive 8.7% in November, blowing analysts' 3.5% prediction out of the water.

Perhaps the greater concern for China is that despite the easing of its zero-tolerance stance, global trade is and will likely continue to retreat, with consumers and businesses slashing their spending. This creates a concerning shift where the problem of supply restrictions - a much easier issue to correct - is beginning to turn into a demand shortage, which is much less controllable.

Getting back to the Rand, after trading sideways for much of the second half of the week, the local unit was trading at R17.13/$ at the opening bell on Friday morning ahead of the final major data release for the week in the form of the US PPI results.

For the year to November, the US producer price index declined to 7.4% from 8.1% in October, while the core PPI also edged lower to 6.2% from 6.7% over the same period. While the report did show inflation continuing to ease, it’s still stubbornly high and clearly isn’t retreating quickly enough to suggest that the US Fed will waiver from its current monetary policy tightening policy just yet.

The initial reaction to the data saw the dollar gathering strength against rivals, and the Rand was no exception, making a swift reversal to close the week in the high-R17.30s, slightly behind where it began.

Which way next for the Rand?

Next week is going to be a telling one.

The Week Ahead (12-16 Dec 2022)

In a relatively thin week of data releases, here’s what we’ll be keeping an eye on over the next five days:

- SA - Mining Production YoY (OCT), Inflation Rate YoY (NOV), PPI YoY (NOV)

- UK - GDP YoY (OCT), Balance of Trade (OCT), Unemployment Rate (OCT), Inflation Rate YoY (NOV), BoE Interest Rate Decision

- EU - ECB Interest Rate Decision, Core Inflation Rate YoY Final (NOV)

- US - Inflation Rate YoY (NOV), Fed Interest Rate Decision, Retail Sales MoM (NOV)

Investors across the globe will be heading into next week nervously as a slew of rate decisions from central banks is expected, chief among which will be the US Fed's, which will undoubtedly take centre stage.

While recent data has signalled that almost a year-long period of rate hikes may be starting to impact prices, the US central bank is widely expected to announce a 50 basis point increase at their final gathering of the year. Like most emerging market currencies, the risk-sensitive Rand remains at the mercy of global drivers, especially US monetary policy…

...and with another rate hike firmly on the cards, it’s fairly safe to say that we can expect major market movement over the next week.

Proceed with caution. It’s shaping up to be a very tricky end to 2022!

How do we navigate these uncertain times?

We'll be relying on our Elliottwave-based forecasts to provide us and our clients with expected direction, enabling better decision-making with more clarity and confidence - and less stress, time and energy.

Please join us as we see out the year safely.

Please take our Rand forecasting service for a test-drive!

This will give you access to the same charts we are to give us and our clients the likely direction of the Rand - ahead of time, enabling you to make educated and informed decision.

Simply use the link below to get access now. No charge. No card. All yours to trial for 14 days.

(You don't want to regret not having done so this time next week...)