CPI Gave. Powell Took. ...42 Cents in One Afternoon.

Published 16 March 2026

Best CPI in years. Worst PPI in months. Same day...

Wednesday started so well...

...the best CPI reading in years landed at 10am. The Rand surged to its strongest level of the month. And for about six hours, it felt like South Africa's story was finally winning.

Then the Fed spoke.

One sentence from Jerome Powell — "inflation isn't coming down as much as we'd hoped" — and the Rand gave back every cent of Wednesday's gains, plus a few extra for good measure.

What followed was two more days of whiplash that left the pair right back where it started... and then some.

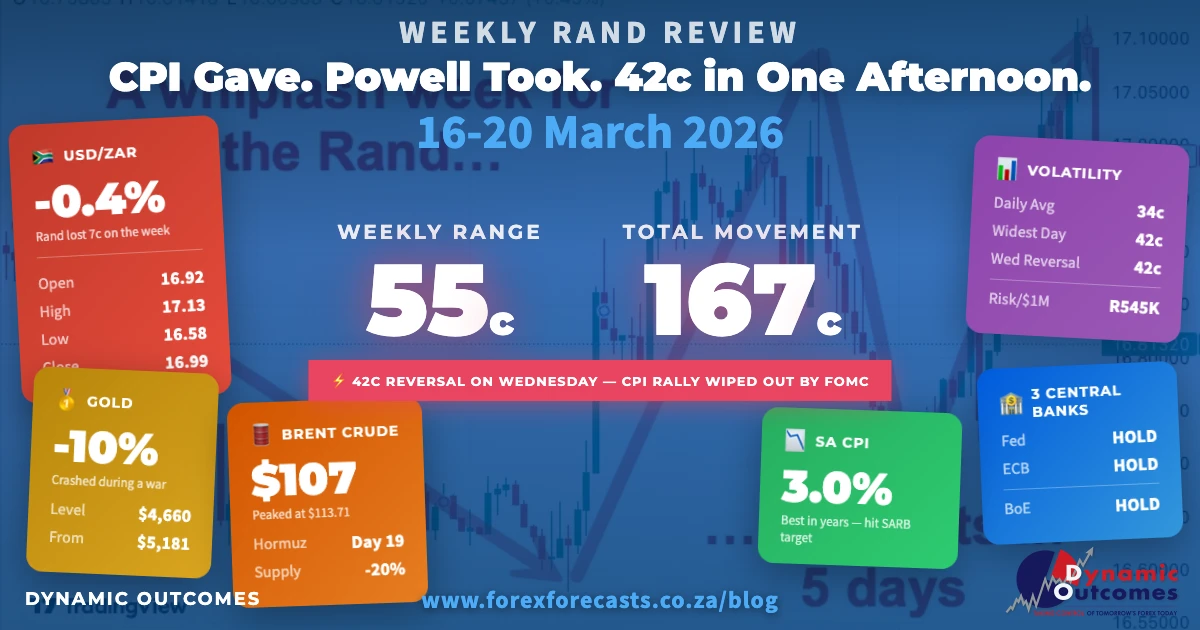

The Rand finished the week at R16.99/$ — roughly 7 cents weaker than Monday's open, with a 55-cent range from R16.58 to R17.13.

Let's dig into how it all played out...

Key Moments (16–20 March 2026)

These were some of the major headlines and events over the past five days:

📊 SA CPI Drops to 3.0%: February inflation fell to 3.0% from 3.5% — below the 3.1% forecast and hitting SARB's new target. Core CPI also at 3.0%. The Rand's best moment of the week.

🚨 US PPI Shocks at +0.7%: Producer prices surged more than double the +0.3% expected — the hottest reading since February 2025. Released the same morning as the FOMC decision. Terrible timing.

🏦 Fed Holds at 3.50-3.75% — Hawkish: 11-1 vote. Dot plot shows only one cut in 2026. Powell: "Inflation isn't coming down as much as we'd hoped." Futures pushed the next cut expectation out to December.

🏦 ECB Holds — Raises Inflation Forecast: ECB kept rates unchanged and raised its 2026 inflation forecast to 2.6% — citing Middle East energy prices. Growth outlook: 0.9%.

🏦 Bank of England Surprise Hold: BoE held at 3.75% unanimously — a cut had been widely expected before the Iran conflict reversed the outlook.

🛢️ Oil Hits $113.71: Brent crude peaked at $113.71 before pulling back to $107.40 by Friday. Strait of Hormuz effectively closed for 19 days now — choking 20% of world oil supply.

📉 Gold Crashes to $4,660: Down from $5,181 on 12 March — a 10% drop in eight days, during a war. Margin calls and dollar strength forced liquidation of safe-haven positions.

🛒 SA Retail Sales Beat Big: January retail trade sales rose 4.2% year-on-year — smashing the +2.5% consensus. Consumer recovery gaining traction.

Monday: A Quiet Rally Nobody Noticed

Monday opened at R16.92/$ and drifted lower through the Asian session...

...nothing dramatic — just a steady leak of dollar strength.

By noon SA time, the pair had dropped to R16.78 as early SA session flows favoured the Rand. The move accelerated through the afternoon — R16.70 by 15:00 SA, R16.65 by 20:00 SA — as thin volumes amplified what was really just positioning ahead of Wednesday's double feature: SA CPI and the FOMC.

The Rand closed at R16.68/$ — a solid 24.5-cent gain on the day, and the strongest close since early the previous week. But nobody was celebrating. Everyone knew Wednesday was coming.

Tuesday: The Calm Before the Storm ️

Tuesday opened at R16.67/$ and went...

...nowhere. A 17-cent range for the entire session. The narrowest day of the week by a mile.

The pair dipped to a low of R16.60 around 15:00 SA time — testing Monday's support — before drifting back to R16.67 by the close. Net move: -0.3 cents. Essentially a rounding error.

Markets were in waiting mode. SA CPI was due Wednesday morning. The FOMC statement Wednesday evening. Nobody wanted to commit before both landed.

(If you've ever watched a market hold its breath for 24 hours straight, this was it.)

Wednesday: The Day of Two Halves

Wednesday was the week. Everything else was prologue and epilogue.

The day opened at R16.66/$ and immediately started testing lower...

...because at 10:00 SA time, Stats SA delivered the number everyone was watching.

CPI: 3.0%. Down from 3.5% in January. Below the 3.1% consensus. And — for the first time — hitting SARB's new 3% target bang on.

The details were equally encouraging. Fuel prices down 10.1% year-on-year. Food inflation eased to 3.7% from 4.4%. Core CPI dropped to 3.0% from 3.4%. Across the board, prices were cooling faster than anyone expected.

The Rand surged. By 11:00 SA time, USD/ZAR had touched R16.58 — the best level of the entire week, and the strongest the Rand had been in weeks. If the day had ended there, this would have been a very different newsletter.

But the day didn't end there.

At 14:00 SA time, the US Bureau of Labor Statistics released February's Producer Price Index...

...and the mood changed instantly.

PPI: +0.7% month-on-month. The market had expected +0.3%. Core PPI came in at +0.5% versus +0.3% expected. Year-on-year, headline PPI sat at 3.4% — the highest since February 2025.

That's not a rounding error. That's a signal. And it landed on the same morning as the FOMC decision.

USD/ZAR spiked from R16.70 to R16.87 in the 14:00 SA hour alone — a 17-cent move in 60 minutes. The CPI rally was already evaporating.

Then came the main event.

At 20:00 SA time, the Federal Reserve released its statement. Rates held at 3.50-3.75% — as expected, with an 11-1 vote (Miran dissented, wanting a cut).

The hold itself wasn't the story. The dot plot was.

The median projection showed just one rate cut for 2026. Seven of nineteen officials saw no cuts at all this year. The inflation forecast was raised to 2.7% (from 2.4% in December). And the longer-run neutral rate ticked up to 3.1%.

Then Powell stepped to the podium.

"Inflation isn't coming down as much as we'd hoped."

That was the sentence. The one that turned a 24-cent Rand rally into a 33-cent rout — in a single afternoon.

USD/ZAR spiked from R16.81 to R16.92 on the statement, then kept climbing through Powell's press conference. By 22:00 SA time, the pair had hit R17.00 — a full 42 cents above Wednesday morning's low.

Wednesday's final score: opened R16.66, closed R16.99. A 42-cent range. And a complete reversal of everything the morning had promised.

In Other News

Three Central Banks, One Answer

It wasn't just the Fed.

In the space of 48 hours, all three of the world's most-watched central banks delivered the same message: not yet.

The Bank of England held at 3.75% on Wednesday — unanimously. A cut had been widely expected before the Iran conflict reversed the inflation outlook. UK GDP was flat in January. Growth is barely registering. But with oil above $100 and the Strait of Hormuz still closed, the BoE couldn't risk adding fuel (quite literally) to the fire.

The ECB followed on Thursday, holding its deposit rate at 2.0% and raising its 2026 inflation forecast to 2.6%. Lagarde was blunt: the Middle East war is creating "upside inflation risk and downside growth risk" simultaneously. The word of the week was "uncertain."

Three central banks. Three continents. Three holds. All driven by the same barrel of oil.

Gold's Uncomfortable Week

Here's the number that should make you pause.

Gold fell from $5,181 on 12 March to $4,660 by Friday — a 10% crash in eight trading days. During a Middle East war. With the Strait of Hormuz closed. With central banks holding rates.

That's not supposed to happen.

Gold is the textbook safe haven. When wars escalate and uncertainty spikes, gold goes up. Except this time it didn't.

Why? The same reason the Rand weakened despite a perfect CPI print: the dollar. DXY climbed to 99.34 on safe-haven flows, making gold more expensive in every other currency. And when equity markets sold off — the S&P 500 hit new 2026 closing lows, the Dow dropped 5.7% in March — margin calls forced liquidation across asset classes. Gold included.

When even gold can't hold its ground during a war, it tells you something about how stressed the plumbing has become.

Eskom: 300 Days and Counting

Closer to home, a milestone that would have been unthinkable two years ago...

...Eskom passed 300 days without load shedding on 12 March.

The Energy Availability Factor sits at 65.85% for the financial year. Unplanned outages are down 53% year-on-year. Diesel spend has dropped R8.58 billion — that's 57% less than the same period last year.

(For anyone who lived through 2023's Stage 6 rotation, this still feels surreal.)

The one risk on the horizon: wage negotiations. Eskom has offered workers a 6.5% increase in the fourth round of talks. The unions haven't accepted. A strike would test the grid at the worst possible time — winter is three months away.

To get back to the Rand...

Thursday: Whiplash in Reverse

Thursday opened at R16.98/$ — still digesting Wednesday's FOMC shock...

...and immediately pushed higher.

Through the early SA session, the pair tested R17.00-R17.02 as markets absorbed the hawkish dot plot and Powell's inflation warning. By 10:00 SA time, sellers had pushed it briefly to R16.88 as some profit-taking kicked in, but the bounce was temporary.

At 14:00 SA time, USD/ZAR spiked to the week's ultimate high — R17.09 — as US session flows amplified the post-FOMC dollar bid. The ECB's hold and raised inflation forecast (released Thursday) added to the pressure.

But then something shifted.

US data started landing — and it was mixed enough to confuse the narrative. Initial jobless claims dropped to 205,000 (below the 215K expected), suggesting the labour market was holding firm. The Philly Fed manufacturing index surged to 18.1 (versus 10.0 expected) — a six-month high. Existing home sales beat at 4.09 million.

The data painted a picture of a US economy that wasn't collapsing — which paradoxically took some of the safe-haven bid out of the dollar.

From 14:00 SA onward, the Rand started clawing back. Steadily, then sharply. By 19:00 SA, USD/ZAR had dropped to R16.88. By 21:00 SA, it touched R16.68 — a 41-cent reversal from the day's high.

Thursday closed at R16.74/$ — 23.8 cents stronger than the open, and a near-complete reversal of Wednesday's damage.

(This is why daily closes matter more than intraday headlines. Thursday's 41-cent range would have made for a terrifying morning if you'd only checked at 14:00.)

Friday: Back to Reality

Friday opened at R16.74/$ — right where Thursday's recovery had landed...

...and it didn't hold.

The early SA session was quiet, with the pair drifting between R16.73 and R16.79 through the Asian and early European hours. But at 11:00 SA time, something broke the peace — a 14-cent spike from R16.81 to R16.95 in a single hour.

By 15:00 SA, the pair was back above R17.00. The US session extended the move — R17.07 by 22:00 SA as oil prices (Brent still above $107) and the broader risk-off tone reasserted themselves.

The week's high came at R17.13 — in the final hours of the New York session — before a late pullback brought the close to R16.99.

Net move on the day: +25 cents of Rand weakness. Whatever Thursday's recovery had achieved, Friday took it back.

The week ended with a familiar lesson: in this environment — oil above $100, central banks frozen, geopolitical risk everywhere — the dollar wins. South Africa can deliver a perfect CPI print, a retail sales beat, and 300 days without load shedding... and it still isn't enough to overcome what's happening offshore.

The US-SA Fault Line

One story that's building quietly in the background — and hasn't fully priced into the Rand yet...

...is the diplomatic crisis between Washington and Pretoria.

US Ambassador Brent Bozell was summoned by DIRCO on 11 March over "undiplomatic remarks." Bloomberg reported that Bozell told SA that Trump's "patience is running out." The ANC has refused to formally recognise Bozell until Ramaphosa accepts his credentials. Ramaphosa, in turn, called Trump "truly uninformed" and "racist."

The demands from Washington are clear: withdraw the ICJ case against Israel, expand the Afrikaner emigration programme, and sever ties with Iran. SA has rejected all three.

Trump has blocked SA from the 2026 G20 summit — scheduled for December at his Doral resort in Florida. SA argues that G20 membership is automatic, not by invitation.

For now, the market shrugs. But this is a ~$20 billion trade relationship. If it escalates from rhetoric to action — tariffs, sanctions, AGOA revocation — the Rand impact would be immediate and significant.

Worth watching.

Volatility and Risk Analysis

This was a volatile week by any measure — but the net result masked the chaos underneath. Roughly R1.67 of cumulative movement across five days... for a net result of 6.6 cents. A 42-cent intraday swing on Wednesday, a 41-cent reversal on Thursday, and two complete direction changes — all to end up almost exactly where it started.

For importers, it was a week of missed opportunities — the Rand's best level (R16.58) lasted roughly six hours before vanishing. For exporters, the return to R17.00+ on Friday offered better conversion levels than anything seen since the previous week.

Open → Close: R16.92 → R16.99 (6.6c / 0.39% weaker)

Average Daily Range: ~34c (0.20%)

Risk per $1 Million Exposure: R342,000

Maximum Single-Day Move: ~33c (2.0%) on Wednesday — CPI-to-FOMC reversal

Risk per $1 Million Exposure: R333,000

Widest Single-Day Range: ~42c on Wednesday (R16.58 to R17.00)

Risk per $1 Million Exposure: R420,000

Weekly Range: 54.5c (R16.58 low to R17.13 high) — 3.2% swing

Risk per $1 Million Exposure: R544,500

The Week Ahead (23–27 March 2026)

SA: SARB MPC rate decision (26 Mar), PPI (26 Mar), ANC "People's March" (21 Mar — Human Rights Day)

US: Consumer Confidence (25 Mar), Durable Goods (26 Mar), PCE Inflation (28 Mar), Michigan Consumer Sentiment final (28 Mar)

EU: ECB minutes review, German Ifo Business Climate (24 Mar)

What to Watch

SARB's dilemma. CPI at 3.0% makes the case for a cut — but oil above $100 makes the case against. Two MPC members voted for a cut in January (when CPI was 3.5%). The question isn't whether the data supports easing. It's whether the SARB trusts that 3.0% will hold when petrol prices catch up to $107 Brent.

Governor Kganyago has warned against complacency. The MPC is split. And Business Day already flagged an April CPI spike from oil. If the SARB cuts into that, it's a bet that transitory energy inflation won't embed. If it holds, it risks keeping rates too tight while the domestic economy struggles at 1.1% growth.

US PCE on Friday. The Fed's preferred inflation gauge lands on 28 March. After PPI's +0.7% shock, markets will be hypersensitive to any upside surprise. A hot PCE print could push rate cut expectations into 2027.

On the forecast front: this week confirmed what the cycles had been signalling — the Rand's strength window is closing as global risk reprices around the Iran conflict. The next few weeks will tell us whether the domestic positives (CPI, retail, Eskom) can hold their own, or whether oil above $100 drowns everything out.

We'll be watching closely.

Until next week – stay sharp...

...and let the market come to you.

Want the full Rand cycle picture?

Register Free for Rand Forecasts