Trump Paused the Bombs. The Rand Surged 58 Cents in Four Hours.

Published 23 March 2026

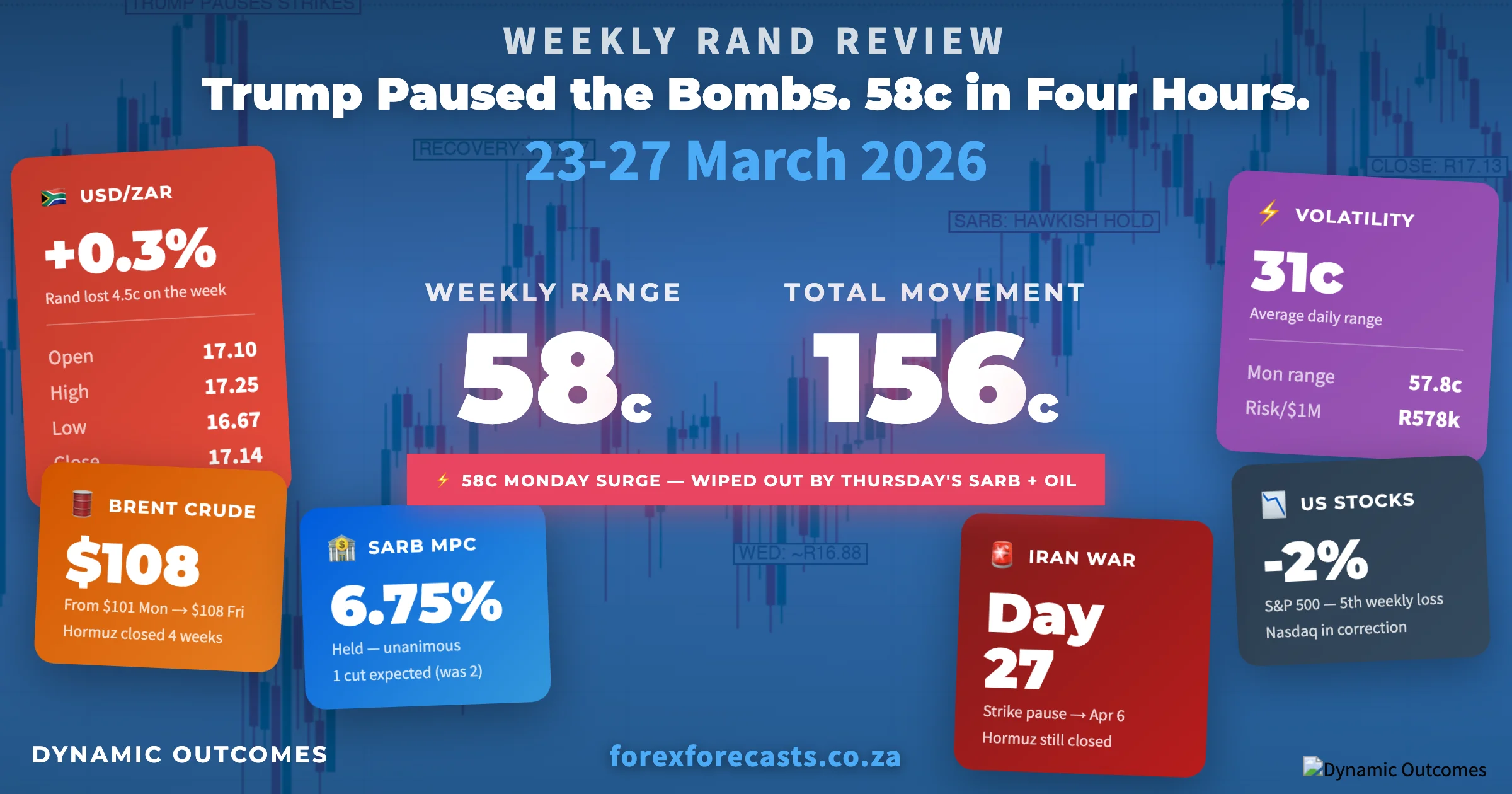

One Trump announcement. 58 cents. Four hours. Here's what happened next...

Monday was extraordinary...

...the kind of day that reminds you why currency markets can be so unforgiving — and so rewarding — in equal measure.

One announcement from Donald Trump — that the US would postpone strikes on Iran's power plants for five days — sent the Rand surging almost 58 cents in a single session. The biggest intraday move of 2026. Risk-on flooded back. Oil dropped. Stocks soared.

And then the rest of the week happened.

The SARB held rates on Thursday and raised its inflation forecast. Oil climbed back above $107. US stocks entered their fifth consecutive week of losses. And by Friday afternoon, every cent of Monday's gains had been handed back...

...and then some.

The Rand finished the week at R17.14/$ — roughly 4 cents weaker than where it started, with a 58-cent range and a cumulative 156 cents of total movement across five days.

Here's how this rollercoaster unfolded...

Key Moments (23–27 March 2026)

These were some of the major headlines and events over the past five days:

🚨 Trump Postpones Iran Strikes: The US president halted military strikes on Iranian power plants for five days after claiming "productive conversations" with Tehran — markets surged on the news.

🏦 SARB Holds at 6.75%: The MPC voted unanimously to keep rates unchanged, raised its 2026 inflation forecast to 3.7% (from 3.3%), and signalled only one rate cut ahead — down from two previously.

📊 SA PPI Falls to 1.8%: February producer prices hit a seven-month low at 1.8% YoY (from 2.2%) — but economists warned the outlook has deteriorated sharply with oil above $100.

🛢️ Oil Surges to $108: Brent crude rose from $101 on Monday to $108 by Friday as the Iran war entered its fourth week and the Strait of Hormuz remained effectively closed.

🚨 Trump Extends Iran Deadline to April 6: On Thursday, the US president pushed back the deadline for strikes on Iran's power grid by another five days — but markets barely reacted the second time.

📉 US Stocks Sink — Fifth Straight Week: The S&P 500 fell ~2% for the week, the Nasdaq confirmed correction territory, and Friday's sell-off deepened on oil and inflation fears.

🗣️ Fed Rate Hike Now in Play: Markets began pricing the Fed's next move as a potential rate hike — not a cut — as oil-driven inflation fears mounted.

Monday: Trump Speaks, the Rand Erupts

Monday opened at R17.10/$ — a gap higher from last week's R16.99 close — and the early hours weren't kind...

...the pair pushed higher through the Asian and early SA sessions, touching R17.25 by mid-morning (the week's high and just 12 cents off last week's peak). Oil fears, Iran tensions, and general risk-off sentiment were all working against the Rand.

Then Trump spoke.

Around 13:00 SA time, the US president announced he would postpone military strikes on Iran's power plants and energy infrastructure for five days. He claimed "productive conversations" with Tehran and suggested both sides wanted a deal.

The market's reaction was instant — and violent.

USD/ZAR dropped from R17.19 to R16.95 in a single hour. By 16:00 SA time it had crashed to R16.67 — the week's low and a move of nearly 58 cents from the morning high. Oil prices fell. US stocks surged (the Dow jumped over 1,000 points). Risk-on sentiment flooded back into emerging markets.

The Rand closed Monday at R16.83/$ — 26 cents stronger than the open, and one of the most dramatic single-day reversals in recent memory.

But here's what made it interesting...

...Iran immediately denied any talks were happening. A senior Iranian official later told CBS News they had "received points from the US through mediators" that were "being reviewed." Not quite the same story.

The market didn't care. By then, the move had been made.

Tuesday: Reality Check

Tuesday opened at R16.86/$ and tried to hold Monday's gains...

...but it was a struggle.

The early session saw the pair drift higher, reaching R16.89 by mid-morning as the initial euphoria wore off. The Iran war was still very much on — this was just a pause, not a resolution. Oil prices started creeping back up. Kuwait warned that the Strait of Hormuz closure was "beyond catastrophic" and would trigger a domino effect across the global economy.

The US session brought more volatility. USD/ZAR pushed up to R17.14 by early evening SA time as crude oil climbed back above $102. The pair see-sawed throughout the afternoon before a late sell-off brought it back to close at R16.91/$ — roughly 5 cents weaker on the day, with a 35-cent range.

The message was clear: Monday's relief rally was a ceasefire, not a peace deal.

Wednesday: The Calm Between Storms ️

Wednesday was the quietest day of the week — and it wasn't even close.

The pair opened at R16.98/$ and closed at R16.98/$. An 18-cent range for the entire session. The narrowest day of the week by a mile.

Markets were waiting. The SARB rate decision loomed on Thursday. SA PPI data was due. US durable goods had been delayed (rescheduled from 25 March to 7 April). And the Iran situation offered nothing new.

It felt like the market was holding its breath...

...and it was.

In Other News

The Strait of Hormuz — Week Four ️

The Strait of Hormuz has now been effectively closed for almost four weeks — and the economic consequences are mounting.

Iran blocked vessel passage after the US-Israeli strikes began on 28 February. This week, Tehran offered a partial olive branch: ships from China, Russia, India, Iraq, and Pakistan would be allowed through. Everyone else? Still blocked.

Trump revealed that Iran's "present" during negotiations was allowing eight oil tankers to pass through earlier in the week. A gesture...

...but not a solution.

Oil tells the story. Brent opened the week at $101 and closed at $108. The journey from $71 in late February to $108 is reshaping everything — from SA petrol prices to SARB policy to the Fed's rate path. And with no resolution in sight, the pressure is only building.

US Stocks — Correction Territory

While the Rand was whipping back and forth, US equity markets were having a quietly terrible week.

The S&P 500 posted its fifth consecutive weekly decline. The Nasdaq officially entered correction territory. Friday's session saw the Dow fall 1.6%, the S&P 1.5%, and the Nasdaq 2.1%.

The driver? Oil and inflation. Markets are now pricing the Fed's next move as a potential rate HIKE — not a cut. The University of Michigan's final March consumer sentiment index fell to 53.3 (from 55.5 preliminary), the lowest reading of the year, with year-ahead inflation expectations jumping to 3.8% — the largest one-month increase since April 2025.

When US stocks sell off this consistently, it usually means risk capital is being pulled from emerging markets too. The Rand felt that pressure from Thursday onwards.

Thursday: SARB Speaks, Oil Screams

Thursday opened at R16.95/$ and the early session was cautious ahead of the SARB's 15:00 SA time announcement...

...but the real action started before the MPC even spoke.

SA PPI landed at 10:00 SA — producer prices fell to 1.8% YoY in February (from 2.2% in January), the lowest reading in seven months. On the surface, great news. But what is the reality? Nedbank raised its 2026 PPI forecast from 2.6% to 3.3%, citing the combination of higher oil prices and a weaker Rand driving up local fuel costs. The good number was backwards-looking. The bad news was coming.

Then the SARB.

Governor Kganyago and the MPC voted unanimously to hold the repo rate at 6.75% (prime at 10.25%). No surprise there — the market had expected it. But the details were hawkish — and then some:

- 2026 inflation forecast raised to 3.7% (was 3.3%)

- 2027 inflation forecast raised to 3.3% (was 3.2%)

- Only ONE rate cut now projected — down from two previously

- Kganyago warned that rate HIKES could be coming — a short war means one hike, a prolonged conflict means multiple

That last point landed hard. How quickly things change! Six months ago the conversation was about how fast the SARB would cut. Now we're talking about hikes. The Iran war has completely rewritten the SARB's playbook.

The Rand weakened steadily through the afternoon. Israel launched strikes on Isfahan and killed the head of the Iranian Revolutionary Guard's navy — the ceasefire mirage was evaporating in real time. Oil surged to $106. Trump extended his Iran strike deadline to April 6 (buying more time, but markets read it as proof no resolution was coming). USD/ZAR climbed from R16.95 to R17.17 before settling at R17.11/$ — the biggest single-day weakening of the week at 17 cents.

Friday: Oil Hits $108, Markets Crack

Friday opened at R17.13/$ and the early session pushed higher...

...testing R17.22 by late morning (just 3 cents below Monday's high). Oil hit $108 per barrel. US stock futures pointed lower. The Iran war intensified — Israel launched new strikes and threatened to "escalate and expand."

The US session brought the week's final blow. Michigan consumer sentiment fell to 53.3 — and more importantly, year-ahead inflation expectations surged to 3.8% (from 3.4%). Oil kept climbing. Stocks sold off hard in the afternoon (S&P and Nasdaq both down over 1.5%). Risk-off sentiment dominated.

The Rand closed at R17.14/$ — essentially where it opened on Monday, making the net weekly move just 4.5 cents of weakening. But the 58-cent range and 156 cents of cumulative movement tell the real story: this was one of the most volatile weeks of 2026.

Volatility and Risk Analysis

What a week for anyone managing currency exposure.

The headline numbers barely tell the story. A 4.5-cent net move sounds boring. But 156 cents of cumulative movement — counting every swing, every reversal, every gap — paints a very different picture. This was the market equivalent of driving 156 kilometres to end up 4 kilometres from where you started. Pretty revealing, isn't it?!

Open → Close: R17.10 → R17.14 (4.5c / 0.26% weaker)

Average Daily Range: ~31.1c (1.8%)

Risk per $1 Million Exposure: R311,000

Maximum Single-Day Range: ~57.8c (3.4%) on Monday — Trump Iran postponement

Risk per $1 Million Exposure: R578,000

Weekly Range: 57.8c (R16.67 low to R17.25 high) — 3.4% swing

Risk per $1 Million Exposure: R578,000

Cumulative Movement: 155.6c across five days

Total intra-week volatility exposure: R1,556,000 per $1M

For importers, Monday's R16.67 was the best buying opportunity in days — but it lasted roughly four hours before vanishing. For exporters, Friday's return to R17.22 offered strong conversion levels. In both cases, timing was everything — and the window was brutally short.

The Week Ahead (30 March – 3 April 2026)

SA: Manufacturing PMI (1 Apr), Vehicle Sales (1 Apr), Absa Business Confidence

US: Consumer Confidence (31 Mar), ISM Manufacturing (1 Apr), JOLTS Job Openings (1 Apr), ADP Employment (2 Apr), Non-Farm Payrolls (3 Apr), PCE Inflation (9 Apr — delayed)

Global: Trump's Iran strike deadline (6 Apr), Strait of Hormuz status, Oil price trajectory

What to Watch

April 6 — the real deadline. Trump's extended pause on strikes against Iran's power grid expires on Monday 6 April. If talks collapse, the US has signalled it will hit Iran's energy infrastructure. If talks succeed (or are extended again), markets will rally — but each extension gets less of a reaction. Monday's 58-cent surge happened on the first postponement. Thursday's extension? Almost nothing. The market is learning to price hope with diminishing returns.

Non-Farm Payrolls on Friday. After the February jobs report shocked markets with a -92K miss (vs +59K expected), all eyes will be on March's number. But as we explored in The Market Demystifier Issue #5 this month — NFP's predictive power for the dollar is worse than a coin flip. The reaction lasts hours, not days. Watch it for the headlines. Don't trade on it.

April's fuel price shock. SA petrol is projected to jump roughly R5/litre to R25.13/L in April, with diesel facing a potential R10/L increase. Add in the additional 21c/L in fuel levies kicking in on 1 April, and the SARB's 3.7% inflation forecast already looks too low. Kganyago's warning about rate hikes isn't theoretical anymore — it's the most likely path if oil stays above $108.

On the forecast front: this week confirmed that the Iran conflict is now the dominant force in Rand pricing. Domestic data (PPI, rate decisions) is being overwhelmed by the oil-war narrative. Until the Strait of Hormuz reopens or a ceasefire holds, expect the Rand to trade more like a war proxy than a fundamentals-driven currency.

We'll be watching closely.

Until next week – stay sharp...

...and let the market come to you.

Want the full Rand cycle picture?

Register Free for Rand Forecasts