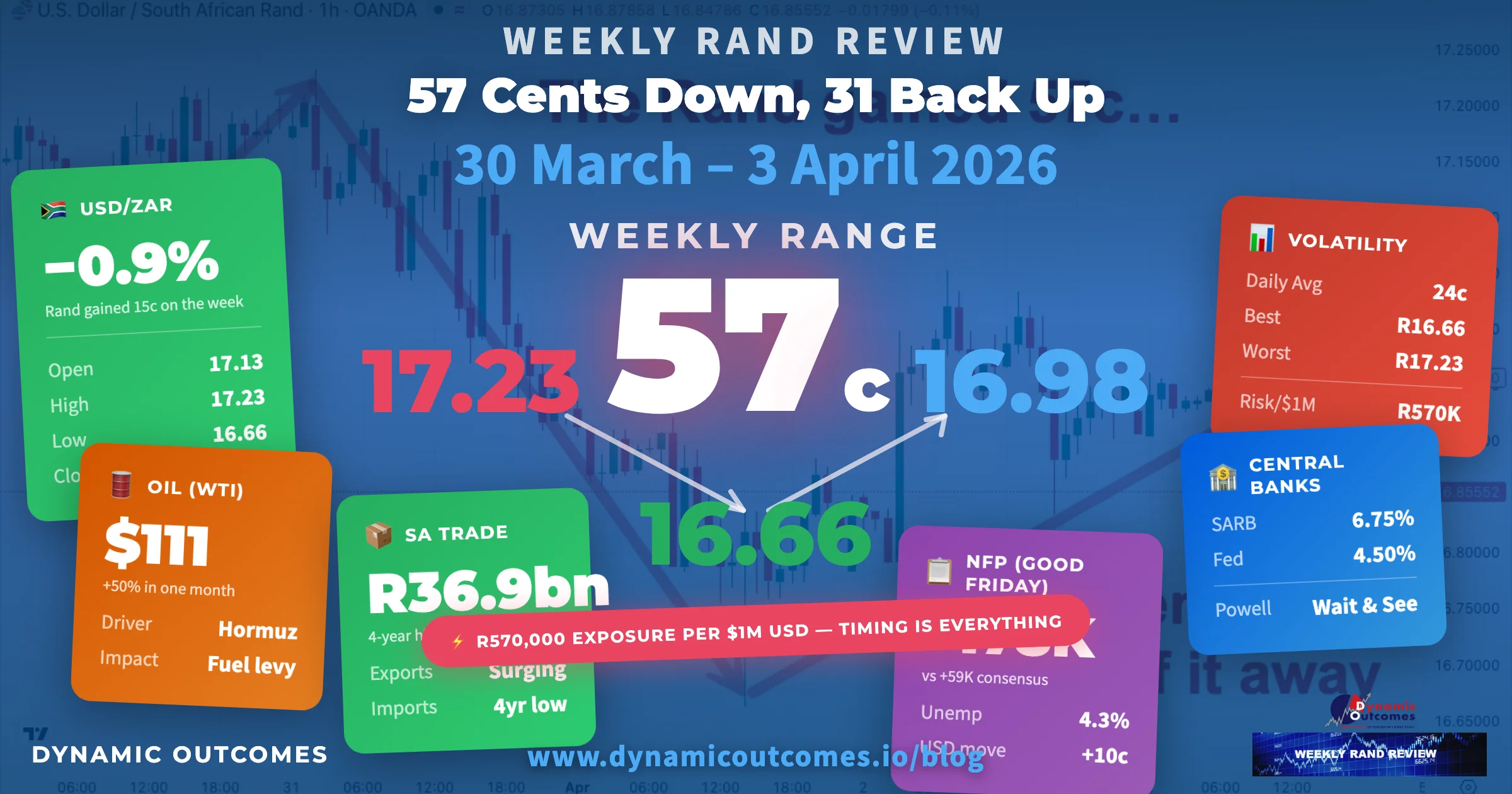

The Rand Gained 57 Cents... Then Gave Half of It Back

Published 30 March 2026

57 Cents Down, 31 Back Up — A Week in the Rand

There's a version of this week where the Rand broke properly lower...

...and everything made sense.

The South African trade surplus hit a four-year high. Quarter-end institutional flows rewired the market in the Rand's favour. Ceasefire hopes sent equities surging and risk appetite flooding back into emerging markets.

For a brief window on Wednesday afternoon, the Dollar/Rand was trading below R16.67 — the best the Rand had been in over five weeks. March's damage, erased in just two sessions.

Then Thursday happened.

And then Good Friday, with the JSE closed, a US jobs report landing on an empty domestic market, and the week's story flipping almost entirely in the wrong direction.

The result? A week that started at R17.13... dipped to R16.66 at its best for the Rand... and closed Friday at R16.98.

A net gain of roughly 15 cents, or about R150,000 per million for importers who were paying attention. But the headline number doesn't begin to capture what happened in between.

Let's dig into how it all played out...

Key Moments (30 March – 3 April 2026)

🏦 Powell at Harvard (Mon): "Wait and see" on tariffs — used 4 times. National debt trajectory: "not sustainable."

🇿🇦 SA Trade Surplus (Mon): R36.9bn in February — 4-year high. Vehicle + metals exports surged; imports at 4-year lows.

📉 Quarter-end + ceasefire flows (Tue–Wed): Institutional rebalancing sent USDZAR to R16.66 mid-week — best Rand level in over five weeks.

🇿🇦 Fuel levy relief (Wed): Government cut R3/litre effective 1 April through 5 May — response to Brent above R1,965/barrel.

⚖️ Liberation Day anniversary (Thu): New 100% pharma tariffs. Existing steel/aluminium tariffs reinforced.

🛢️ Oil surge (Thu): WTI through $111/barrel — up 50%+ in a month on Strait of Hormuz disruptions.

📊 NFP — Good Friday (Fri): +178,000 vs +59,000 consensus. Dollar nudged — didn't surge. JSE closed, thin market.

Monday 30 March: Powell Weighs In, and the Rand Holds Steady

Before the market even opened, our Rand Forecast subscribers already had a framework for the week ahead.

Our short-term cycle analysis, issued Friday 28 March, identified a topping pattern in USDZAR. Sentiment cycles were pointing to Rand recovery. The key confirmation level: a sustained break below R16.50, with a target zone of R16.30–R16.50.

In other words — while the headlines were still full of doom about March's selloff, our cycle work was already saying: the turn is close.

Based on the above, it looked like it was going to be an interesting week.

The week opened with Federal Reserve Chair Jerome Powell taking the stage at Harvard — and the market listening carefully.

Powell's message was measured. The US economy was holding up. Inflation expectations were "well-anchored." But on two things he was direct: the trajectory of the national debt was "not sustainable," and on tariffs, the Fed's position remained "wait and see."

(For what it's worth, that phrase — "wait and see" — appeared four times across Powell's Harvard remarks. Markets have learned to read its subtext. The Fed is watching, but it's not moving.)

Back home, a quietly significant data point landed on Monday morning. South Africa's February trade surplus came in at R36.9 billion — the strongest reading in years, driven by a surge in vehicle and metals exports and a collapse in imports to four-year lows.

It's not the kind of number that moves the market on its own...

...but it matters.

A strong trade surplus means Rand is coming into the country. It's a structural support that often gets overlooked when the headlines are all about tariffs and geopolitics.

The Rand spent the day ranging between R17.03 and R17.22 — briefly touching the stronger side in the early Asian session before pulling back as the US opened.

It closed Monday at R17.18, fractionally weaker than Friday's close.

Steady, but not convincing.

USDZAR: Open 17.1283 | High 17.2180 | Low 17.0355 | Close 17.1789 | Net: +5 cents 📈

Tuesday 31 March: Quarter-End Does What Quarter-End Does

If there's one thing institutional money does reliably at the end of every quarter, it's rebalance.

After a brutal March for global equities — the S&P 500 down 5.1%, the Dow falling 5.2% (its worst monthly performance since September 2022) — pension funds, asset managers, and institutional desks needed to sell winners and buy laggards.

And in a month where EM currencies had been hammered by tariff fears and oil-price shock, the rebalancing trade pointed in one direction: sell dollars, buy rand.

That's the mechanical explanation.

But there was a narrative catalyst too. Rumours of a US-Iran ceasefire — however tentative — swept through markets Tuesday morning. The Dow surged 1,125 points.

Risk appetite flooded back in a way markets hadn't seen in weeks...

...and the Rand flew!

By Tuesday afternoon, USDZAR had plunged from its overnight high of R17.23 all the way to R16.91 — a 320-pip move in a single session.

Month-end, quarter-end, ceasefire hopes, and a trade surplus still fresh in memory. The rand caught every tailwind available.

It closed Tuesday at R16.94. The strongest one-day Rand move of the quarter.

(March 31 also marked the end of South Africa's fiscal year. There's always some domestic rand demand around this date from companies squaring off foreign currency positions.)

Another quiet tailwind that doesn't make the headlines but shows up in the price.

USDZAR: Open 17.1963 | High 17.2330 | Low 16.9095 | Close 16.9425 | Net: −25 cents 📉

Wednesday 1 April: The Rand Hits Its Best Level in Five Weeks

If Tuesday was the spark, Wednesday was the bonfire.

The Rand opened April 1 around R16.96 and didn't look back.

By early afternoon — around the time the JSE lunch session was wrapping up — USDZAR had traded down to R16.6625.

That's the strongest the Rand had been since late February — before the Hormuz crisis blew the market wide open.

For importers with dollar payables, it was a gift — roughly R570,000 cheaper per million than Tuesday's high. For exporters, it was painful. Either way, it was a number worth writing down.

What drove it? A combination of factors, none of them individually decisive, but collectively overwhelming.

The ceasefire optimism from Tuesday hadn't fully faded. US manufacturing data came in stronger than expected — ISM at 52.7%, the highest reading since August 2022. The US economy was absorbing the tariff shock better than feared.

ADP employment figures for March came in at +62,000, above the 40,000 forecast. Both readings were consistent with a "soft landing" narrative that tends to be risk-positive.

And then, from Pretoria, the government announced a R3 per litre temporary reduction in the fuel levy — running from 1 April to 5 May.

The measure was a direct response to Brent crude's surge above R1,965 per barrel (in Rand terms), driven by Strait of Hormuz disruptions. A government stepping in to cushion the oil price shock is exactly the kind of policy response that steadies confidence — and, marginally, the currency.

The Rand didn't hold R16.66. Markets rarely hand you the cleanest levels for long.

By Wednesday's close, USDZAR had retraced to R16.81. But the message was clear: the underlying bid for the rand hadn't gone away.

USDZAR: Open 16.9624 | High 16.9624 | Low 16.6625 | Close 16.8136 | Net: −15 cents 📉

In Other News...

SA-US trade tensions deepening

The South African Reserve Bank formally noted in a report this week that Trump's tariffs have "significantly reduced" South Africa's exports to the United States.

Automotive exports — once a cornerstone of SA's manufacturing export story — have fallen by approximately 75% since the tariff regime was introduced.

AGOA has been extended through December 2026, but with a Section 122 surcharge that largely negates the preferential pricing. The strategic pivot to China — Chinese Vice President Han Zheng visited Pretoria this week, and China is introducing zero tariffs on 53 African nations from May 1 — reflects where SA is repositioning itself...

...but as we have said before, Beijing never does anything without ensuring that it will get its pound of flesh (and more) out of any deal.

PMI edges higher but stays in contraction

The Absa Manufacturing PMI came in at 49.0 for March — up from February's 47.4, but still in contraction for the sixth consecutive month.

More concerning: the expectations index collapsed 22.9 points to 45.9 — a record single-month drop. Input costs are surging on the back of a weaker Rand and oil prices.

The improvement in the headline number masks a deteriorating sentiment picture.

Eskom tariff hike takes effect

A further 8.76% tariff increase on direct Eskom customers came into effect on 1 April. This is separate from the general tariff increase approved for municipalities — direct-supply industrial and commercial customers absorb this hike immediately.

Against the backdrop of 300+ consecutive days without load shedding — a genuine structural improvement — the tariff pressure is the new inflation risk the SARB is watching.

Which brings us back to Thursday — and the moment the week's optimism unravelled.

Thursday 2 April: Liberation Day's Anniversary, and the Reversal

A year ago, Donald Trump stood in the Rose Garden and announced sweeping global tariffs in what his administration called "Liberation Day."

Thursday, April 2, 2026 was the anniversary.

And the White House — never one to let a symbolic date pass unused — used it.

New pharmaceutical tariffs at 100% were announced for imports from countries not offering "reciprocal" market access. The existing 50% tariffs on steel and aluminium remained, with new enforcement mechanisms.

The Rand, which had spent two days strengthening on the back of ceasefire hopes and quarter-end flows, immediately came under pressure.

But it wasn't just the tariff headline.

Oil. WTI crude surged through $111 per barrel on Thursday — up more than 50% from a month ago — as fresh reports emerged of shipping disruptions in the Strait of Hormuz.

For South Africa, an oil importer running a current account already under pressure from US trade policy, $111 oil is not an abstract number. It feeds directly into the petrol price, into inflation, into the SARB's rate calculus.

(It's worth noting that the SARB had earlier cited oil's surge — specifically Brent above R1,965 per barrel — as a key reason for holding the repo rate at 6.75%. The government's fuel levy relief buys a few weeks. But it doesn't change the structural pressure.)

The Rand reversed sharply. From an open of R16.79, USDZAR pushed through R17.05 during the morning session before settling back to R16.95 by the close.

In a single day, most of Tuesday's gains were given back.

USDZAR: Open 16.7850 | High 17.0530 | Low 16.7813 | Close 16.9497 | Net: +16 cents 📈

Friday 3 April: Good Friday, a Jobs Beat, and Thin Trading

The JSE was closed on Good Friday.

South African markets were quiet in the domestic session — but that didn't mean USDZAR was standing still. International markets traded as normal, and at 14:30 SAST, the Bureau of Labour Statistics dropped the March Non-Farm Payrolls report.

The result: +178,000 jobs added in March. Against a consensus forecast of +59,000.

Makes sense that a 119,000-job beat would send the dollar higher, right? But what is the reality?

We devoted an entire issue of The Market Demystifier to dismantling the NFP myth — the idea that the "most important economic release in the world" actually drives the dollar in a predictable, reliable way.

Our analysis showed NFP explains at most 16% of dollar movement on release day. In February, the US lost 92,000 jobs on the initial release — since revised to -133,000 — and the dollar went up.

This Friday, the dollar also went up on a big beat. So you might conclude the NFP-dollar relationship is back to working.

But here's the nuance: the dollar didn't surge. USDZAR moved from R16.93 to just above R17.01 on the news — a 10-cent move in an extremely thin market.

The underlying USD didn't go on a rampage. It added to the Thursday reversal, locked in a close above R17.00, and left the week's net move at a modest 12-cent Rand gain...

...mostly built on Tuesday and Wednesday before it all came apart.

Intriguing, isn't it?

Pretty revealing, actually.

The unemployment rate ticked down to 4.3%. Wages came in below expectations at +3.5% year-on-year — the piece the Fed will actually focus on. A wages softening story is consistent with one rate cut pencilled in for 2026.

By 17:00 SAST, USDZAR had settled at R16.98. The Rand closed the week stronger than it opened — but the margin was modest given the 57-cent range it carved along the way.

USDZAR: Open 16.9275 | High 17.0197 | Low 16.9049 | Close 16.9765 | Net: +3 cents 📈

Volatility and Risk Analysis

This was a week defined by the gap between what almost happened and what actually did. A 57-cent range in five trading days — nearly R570,000 of exposure per $1 million. Here's the breakdown:

Open → Close: R17.1283 → R16.9765 | Net: −15 cents (Rand stronger)

Best for Rand: R16.6625 — Wednesday afternoon

Worst for Rand: R17.2330 — Tuesday night

Weekly Range: 57 cents | Risk: R570,000 per $1M

Daily Average Range: 24 cents | Risk: R240,000/day per $1M

Rand vs Major Currencies (30 March – 3 April 2026)

- USD/ZAR: Open 17.13 → Close 16.98 | Move: −15c | −0.88% | Range: 57c (16.66–17.23)

- EUR/ZAR: Open 19.72 → Close 19.60 | Move: −12c | −0.59% | Range: 41c (19.36–19.77)

- GBP/ZAR: Open 22.72 → Close 22.46 | Move: −26c | −1.12% | Range: 48c (22.29–22.77)

Rand strengthened against all three majors on the week. Largest gain vs GBP (−1.12%). GBPZAR also had the biggest range (48 cents).

If you have $1 million in USD payables, this week's range represented R570,000 of potential variability in your ZAR cost. It all depended on which day you transacted.

A company that bought dollars on Tuesday morning paid R530,000 more per million than one that waited until Wednesday afternoon.

That's not analysis. That's real money.

For importers — who need a strong Rand (lower USDZAR) — Wednesday's R16.6625 low was the best buying window of the week. Arguably the best of the year so far.

Whether your treasury team was positioned for it is a separate question.

For exporters — who benefit from a weak Rand (higher USDZAR) — Monday and Thursday both offered relative windows.

But with oil at $111 and Brent above R1,965/barrel, the underlying cost pressure in your supply chain is rising faster than the Rand rate is helping.

Rand Forecast Snapshot

On Friday 28 March, we issued short-term outlooks on all three Rand pairs — USDZAR, EURZAR, and GBPZAR. All three called the same thing: topping patterns, with further downside ahead.

Here's how the week played out against those forecasts.

USDZAR came within 6 pips of triggering the next leg lower.

The forecast identified R16.60 as the key confirmation level — a break below which would have pointed the market toward the R16.30 target zone. Wednesday's low of R16.6625 got there...

...and then Liberation Day happened.

The tariff announcements on Thursday pushed USDZAR back above R17.00 before the confirmation could fire.

The directional call remains intact — the updated forecast issued Wednesday continues to target further downside — but the move hasn't confirmed yet. Six pips separated the market from a clean validation.

EURZAR and GBPZAR both delivered the move.

EURZAR dropped 35 cents from the forecast price to its week low of R19.36.

GBPZAR moved 51 cents — from R22.71 at forecast time to a low of R22.20 on Wednesday, confirming the downside direction cleanly.

Three forecasts, three correct directions. USDZAR remains the one to watch — the confirmation level at R16.60 is still live.

If you want to see how this plays out — or to look back at how our forecasts have tracked over time — the full track record is available at portal.dynamicoutcomes.io/track-record.

The Week Ahead (6 – 9 April 2026)

A shortened week. Easter Monday (6 April) is a public holiday in South Africa, so the JSE opens Tuesday. International markets are broadly open Monday, though European volumes will be lighter.

- SA: Easter Monday holiday (Mon 6 Apr). JSE opens Tuesday.

- US: FOMC Minutes — est. Wednesday 8 April | US CPI (March) — Thursday 10 April

- Watch: Oil price vs SARB repo threshold | US-Iran ceasefire developments

What to Watch

FOMC Minutes (est. Wednesday 8 April): The minutes from the March 17-18 Fed meeting — at which the Fed held rates at 3.50-3.75% with one dissenter.

Markets will parse the discussion around tariffs, the inflation outlook (ISM Prices Index at 78.3%, highest since June 2022), and signalling around that single projected 2026 rate cut.

US CPI (Thursday 10 April): March inflation data. Coming off ISM Prices surging to 78.3% and oil at $111/barrel, the headline number could surprise higher.

The Fed's "wait and see" posture on tariffs gets tested immediately by what the data shows.

SARB & Oil: Repo rate held at 6.75%. The government's R3/litre fuel levy relief runs to 5 May.

Watch whether Brent crude sustains above $100 per barrel — every dollar above that level erodes the relief measure's effectiveness and moves the dial toward the SARB having to act later in the year.

US-Iran: The ceasefire rumours that drove Tuesday's equity surge have not materialised into formal agreements.

Trump has set a hard deadline of 8pm ET Tuesday 8 April for Iran to reopen the Strait of Hormuz — calling it "final." Iran has rejected the proposed 45-day ceasefire and countered with a 10-clause proposal that includes a permanent end to hostilities.

As of writing, both sides are in a hardened standoff. Any escalation — or credible deal — is the single largest variable for the Rand this week.

Until next week — stay sharp, stay sceptical, and don't let the headlines do your thinking for you.

P.S. NFP came in at 178,000 against a 59,000 consensus. A massive beat.

And the dollar... nudged. It didn't surge.

That distinction matters — and it's the same pattern we see over and over again.

Oil, tariffs, ceasefire hopes, quarter-end flows — they all play a role. But none of them explain why the Rand swung 57 cents from peak to trough — or why it snapped back 31 cents just as fast.

What does? Sentiment cycles. The same cyclical structures that had our subscribers positioned for a Rand recovery before Monday's open.

In Issue #5 of The Market Demystifier, we dismantled the NFP myth — showing that it explains at most 16% of dollar movement on release day.

The other 84% isn't a random collection of headlines. It's sentiment, moving in cycles, and it's measurable. That's what we do at Dynamic Outcomes.

"Oil, tariffs, NFP, ceasefire hopes — they all played a part. But none of them explain a 57-cent swing from peak to trough — or the 31-cent snap back. Not even close. Sentiment cycles do. And they're measurable."

USDZAR data sourced from OANDA API. All price levels verified against live data. Weekly range: 16.6625–17.2330 (57 cents). Net move: −15 cents (Rand stronger on week).

Want the full Rand cycle picture?

Register Free for Rand Forecasts