The Rand Just Had Its Best Week of 2026...

...and It Took a Ceasefire and a Tariff Pause to Get There

Published 6 April 2026

This was the week the dominoes fell...

...in the Rand's favour.

Two geopolitical shockwaves — landing 48 hours apart — rewrote the script on the Dollar/Rand in a way we haven't seen all year. The kind of week where importers checking their rates on Monday morning and again on Wednesday afternoon would have thought they were looking at a different currency pair.

And buried underneath the headlines? A US inflation print that should have rattled markets...

...but barely moved the needle.

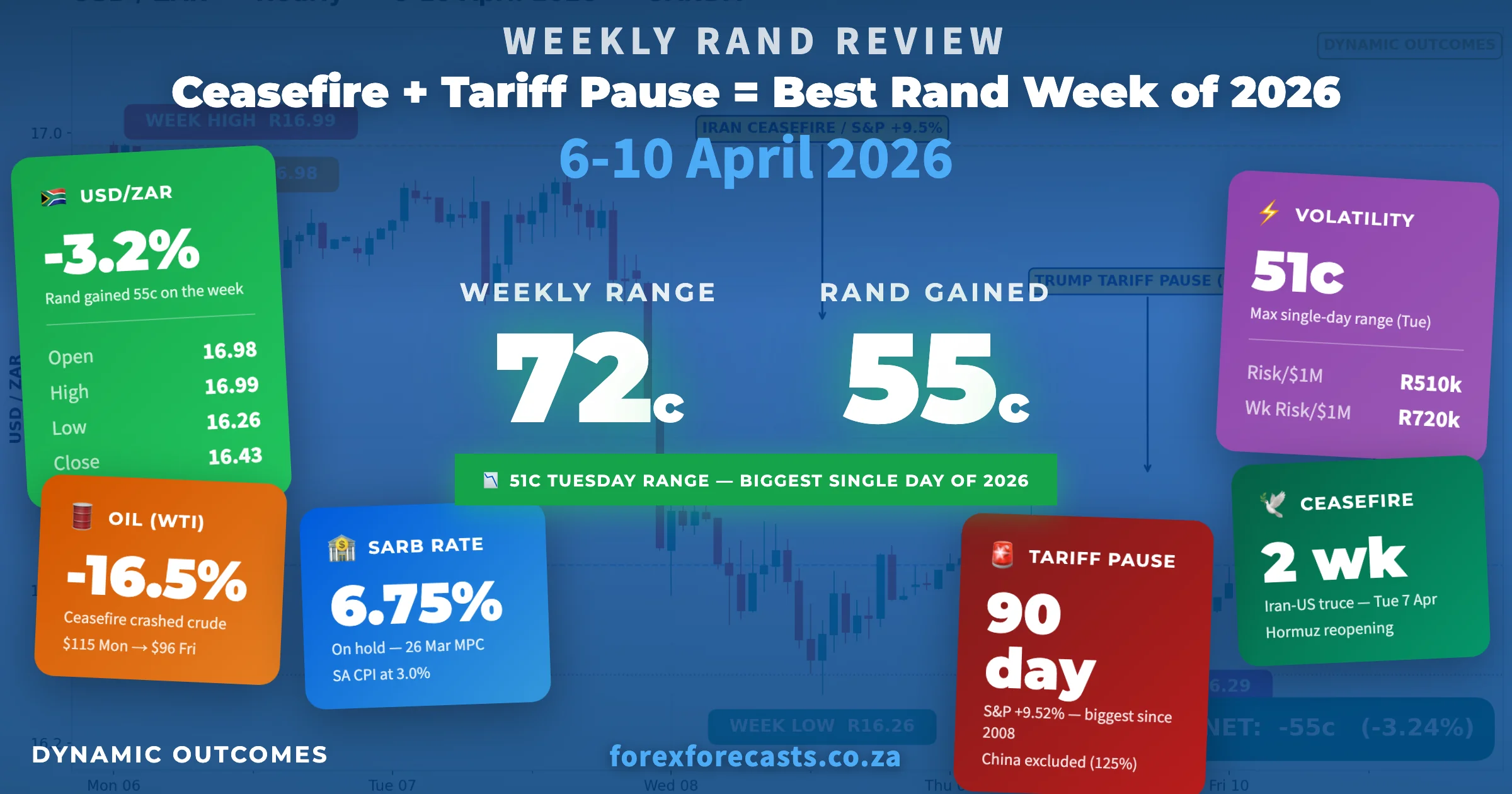

The result? The Rand strengthened from R16.98/$ on Monday's open to close the week at R16.43/$ — a gain of roughly 55 cents, or about R550,000 per million dollars of exposure.

Here's how this rollercoaster unfolded...

Key Moments (6 – 10 April 2026)

🚨 Iran-US Ceasefire Lands Tuesday: Two-week truce mediated by Pakistan — Strait of Hormuz reopening, WTI crude crashes 15% in a single session to close the week at $95.99 (-16.5%)

🚨 Trump Pauses Reciprocal Tariffs for 90 Days: Thursday's Truth Social bombshell spared every country except China (which got hit harder at 125%) — S&P 500 surged +9.52%, its largest single-day gain since 2008

📊 US CPI Surges 0.9% in March: Friday's print was the biggest monthly jump since June 2022, driven by a 21.2% gasoline spike (largest since the BLS series began in 1967) — but core CPI tame at 0.2%

📉 Michigan Sentiment Crashes to All-Time Low: 47.6 preliminary April reading — 1-year inflation expectations surge from 3.8% to 4.8%

📉 SA Manufacturing Contracts -2.2% MoM: February output significantly worse than expected (4th consecutive YoY fall) — barely registered in the week's risk-on rally

🇿🇦 Eskom Redeems R38 Billion ES26 Bond: Landmark milestone for SA's power utility — combined with 300+ days no load shedding, quiet structural progress continues underneath

Monday 6 April: Steady Start, Markets Watching ️

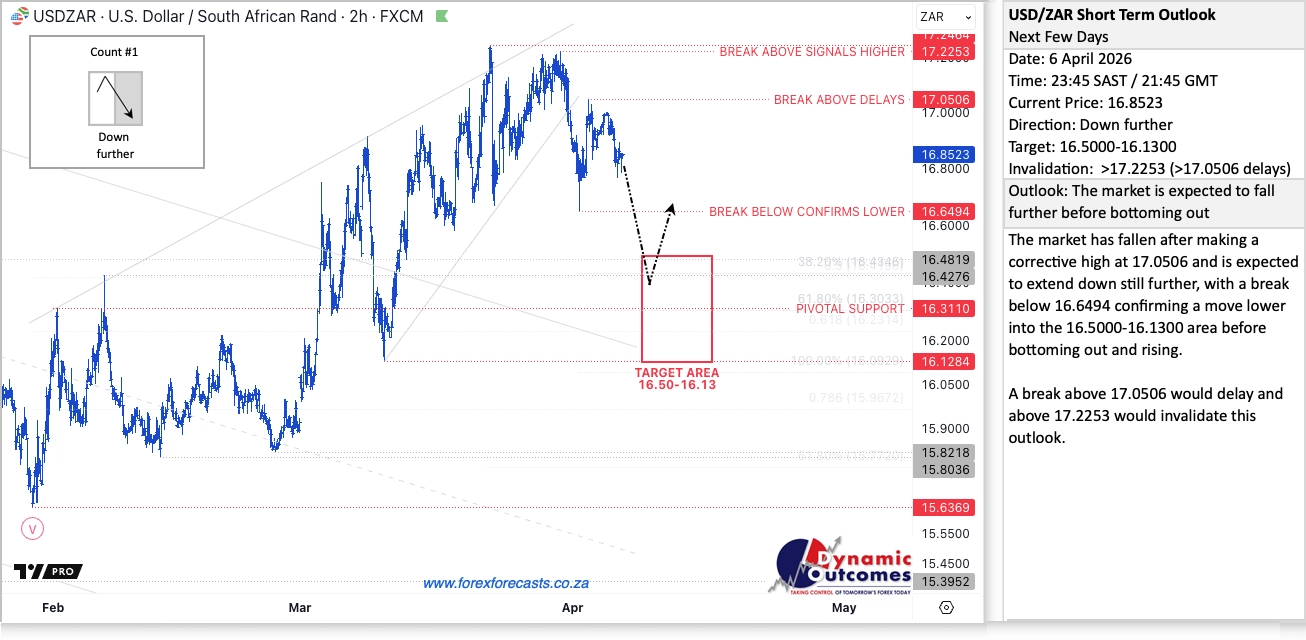

The Forecast: Before the week began, our USDZAR short-term outlook — issued Monday 6 April — was calling for further downside. The target zone: R16.50–R16.13. Direction: down.

We didn't know what news would trigger this move, but sentiment was expected to take it there on our cycle work...

The week opened at R16.98/$ and the early session saw cautious trade...

...with the pair drifting in a tight range between R16.77 and R16.99.

Monday's story was one of positioning. The geopolitical landscape was loaded — the Iran-US conflict was entering its sixth week, oil prices remained above $110/barrel, and the country-specific reciprocal tariffs were due to kick in later in the week.

On the domestic front, Eskom quietly made history. The power utility redeemed its landmark R38 billion ES26 bond — a milestone for financial sustainability and, frankly, something most people would have laughed at three years ago.

Combined with 300+ days without load shedding, it's the kind of boring, structural progress that won't make front pages but keeps the Rand supported underneath.

The Rand spent most of Monday trying to find its footing. Some early weakness pushed the pair up to test R16.99 — which would prove to be the week's high — before settling back.

The close came in at R16.87/$ — an 11-cent gain from the open, but nothing to write home about.

Not yet, anyway.

Tuesday 7 April: Ceasefire Shock Rewrites Everything

Tuesday opened at R16.87/$ and immediately...

...the rules changed.

On the data front, the S&P Global SA Composite PMI for March came in at 50.8 — the first real expansion in six months after a prolonged stretch in contraction territory. A quiet positive for the SA economy, even if the headlines were looking elsewhere.

But the bigger story was geopolitical. News broke that the United States and Iran had agreed to a two-week ceasefire, mediated by Pakistan. The terms: a halt to US military strikes, the "complete, immediate and safe opening" of the Strait of Hormuz, and a framework for broader negotiations.

The Strait of Hormuz — the chokepoint for one-fifth of the world's oil and gas — had been effectively closed since Iran shut it in retaliation for the US-Israeli military campaign launched on 28 February. The closure had choked off a huge slice of global crude supply...

...one of the biggest oil supply disruptions on record.

And now, in one announcement, the pressure valve opened.

Oil prices cratered. WTI crude dropped from $114.51 to $97.02 in a single session — a 15% crash, the largest one-day move since the war began. By Friday, WTI closed the week at $95.99 per barrel, having touched an intraday low of $91.60 on Tuesday. Brent followed the same path. The week's net move in oil: -16.5%.

(A 15% single-session crash. You don't see those often — and almost never for bullish reasons.)

For context, pre-war levels were around $70 — so we're still materially above normal — but the direction of travel was unmistakable.

(The ceasefire was fragile, mind you. Iran's Revolutionary Guard reported that Strait shipping had stopped again hours later, after Israeli strikes in Lebanon which they considered a violation. But markets had already priced in the relief.)

The Rand did the rest. USD/ZAR slid from R16.87 to R16.46 through the session — a 41-cent drop in a single day. The move was relentless...

...the explosion was coming Thursday.

Wednesday 8 April: Low of the Week

Wednesday opened at R16.45/$ and for a few hours in the early Johannesburg session, things looked almost orderly.

Back home, Stats SA released February manufacturing production data: -2.2% month-on-month, -2.8% year-on-year — the fourth consecutive YoY decline. A significant miss against consensus. The factory sector is in contraction. Adding to the drag, SARB's forex reserves dropped from $81.01 billion to $77.76 billion.

In normal times, both would have pressured the Rand. This week? They barely registered.

By mid-morning, USD/ZAR was testing fresh lows. The pair punched down to R16.26 — the low of the week — before finding a floor.

At the same time, the Federal Reserve released its March FOMC meeting minutes. The tone was cautious. Inflation remained above the 2% target. The Iran oil shock added "elevated uncertainty." Markets read it as dovish...

...which only reinforced the dollar's slide.

Globally, the ceasefire relief was being celebrated in the stock indices. The S&P 500 climbed 2.51% on the day, the Dow added 2.85%, the Nasdaq rose 2.80%. Risk appetite came flooding back. The Dollar weakened against everything.

Bloomberg called it explicitly: "South Africa leads EM rebound as de-escalation trade takes hold."

New US Ambassador to South Africa Mark Bozell was also accredited that day — replacing the previous envoy after SA expelled the former ambassador last year over what Pretoria called a "white victimhood" narrative. The bilateral relationship remains fractured, but at least there's now a face at the Embassy again.

Wednesday closed at R16.43/$ — essentially stable from the morning after touching the week's low.

The bigger fireworks were still to come.

In Other News...

Iran Ceasefire: Relief or Reprieve?

The Tuesday-Wednesday ceasefire was the headline — but the fine print deserved closer reading.

Hours after the agreement was announced, Iran's Islamic Revolutionary Guard reported that shipping through the Strait of Hormuz had stopped again, citing Israeli strikes in Lebanon as a violation of the truce.

The US and Iran remain "poles apart" on what a comprehensive agreement would look like. Washington wants complete denuclearisation. Tehran wants sanctions lifted. Neither seems ready to budge.

Oil may be below $100 today...

...but we're still materially above pre-war levels. And the ceasefire has a two-week expiry.

Trump's Tariff Tango: Pause, Not Peace ️

The 90-day pause on reciprocal tariffs was celebrated like a victory — and for markets, it was. But the details matter.

The 10% baseline tariff remains in place for everyone. China's rate went UP, not down — to 125%. And the pause was born not of conviction, but of market panic. Reports emerged that Bessent and Lutnick had lobbied Trump directly after stocks tanked, convincing him to reverse course while Navarro was out of the room.

For South Africa, the pause means 90 more days at 10%. But the underlying tensions — the broader Trump-Pretoria frustrations, the AGOA questions, the geopolitical positioning — haven't gone anywhere.

Trump-SA Relations: New Ambassador, Same Tensions

The bilateral relationship between Pretoria and Washington remains fractured — and this week brought fresh reminders.

New US Ambassador Mark Bozell was accredited on Wednesday, replacing the previous envoy after SA expelled the former ambassador over the "white victimhood" narrative. AGOA has been extended through December 2026, but it's not exempt from the reciprocal tariffs. So the 10% baseline still bites, and the structural trade relationship remains on shaky ground.

SA's Triple Price Shock Arrives

April brought a "triple price shock" for South African consumers and businesses: fuel prices surging on the Iran war premium, an 8.76% electricity tariff hike effective 1 April, and a carbon levy increase.

Headline CPI sits at 3.0% (February reading) — sitting right at the new SARB target midpoint under the revised regime — but the SARB flagged these pressures explicitly at its March meeting. If oil stays elevated and the electricity hike feeds through, a short-term breach above 4% isn't out of the question.

The silver lining? The repo rate at 6.75% gives the SARB room to hold — or even cut — if global conditions stabilise. The ceasefire and tariff pause both help on that front.

The Ramaphosa Pivot

South Africa's pivot east isn't slowing down — it's accelerating. The CAEPA framework signed earlier this year with China (by Trade Minister Tau) handed SA agricultural exporters preferential access to the Chinese market, and the rhetoric coming out of Pretoria this week made the direction unmistakable.

This isn't a pragmatic hedge against US trade uncertainty...

...it's an ideological doubling-down. The ANC/SACP alliance is openly comfortable aligning with Beijing, Moscow, and the broader BRICS+ bloc — fellow travellers on the communist end of the political spectrum. Whether that serves ordinary South Africans is a different question entirely.

Thursday 9 April: The Day Everything Broke

Thursday opened at R16.43/$ with markets already digesting two days of relief...

...when the biggest shock of the week landed.

Earlier in the morning, the Bureau of Economic Analysis released its third estimate for Q4 2025 GDP: +0.5% annualised, revised down 0.2 percentage points. The US economy was slowing. The Atlanta Fed's GDPNow tracker had Q1 2026 at just +1.3% — down from +1.9% at the start of the month.

Then, at approximately 13:00 ET (19:00 SA time), Donald Trump posted on Truth Social. Reciprocal tariffs above 10% — which had gone into effect hours earlier — would be paused for 90 days. For every country except China.

China, meanwhile, saw its tariff rate jacked up to 125%.

The market's reaction was instantaneous. And violent.

The S&P 500 surged 9.52% on the day — its largest single-day gain since 2008. The DXY dollar index crumbled below 99. Every risk asset on the planet caught a bid.

(Inside the room: reporting from the Washington Examiner confirmed what many suspected — Treasury Secretary Bessent and Commerce Secretary Lutnick had lobbied Trump directly, convincing him to reverse course while trade hawk Peter Navarro was deliberately kept in a separate meeting. The diplomatic term for this is "tactical flexibility." The market term is "he blinked.")

For South Africa specifically, the pause means the rate stays at the 10% baseline for another 90 days. That's not free trade — but the alternative (the pre-SCOTUS 30% figure returning through a different legal route) is a conversation no exporter wants to have.

The Rand? It traded in a tight range as the Dollar selloff broadened globally — closing at R16.39/$, another 4 cents stronger.

For those keeping score: from Monday's open at R16.98 to Thursday's close at R16.39, that was 59 cents of Rand strength in four trading days.

Friday 10 April: CPI Day — Hot Print, Cool Reaction

Friday opened at R16.39/$ and the market was still digesting Thursday's earthquake...

...when another data bomb landed.

The Bureau of Labor Statistics released March CPI at 14:30 SA time. The headline: consumer prices surged 0.9% month-on-month — the biggest monthly jump since June 2022. Year-on-year, inflation hit 3.3%.

The culprit? Gasoline. Pump prices spiked 21.2% in March — the largest monthly increase since the BLS series began in 1967 — accounting for nearly three-quarters of the entire CPI move. The Iran war's oil shock was now showing up in the hard data.

But here's the nuance the headlines missed...

...core CPI (stripping out food and energy) rose just 0.2% for the month, with the annual rate ticking up modestly to 2.6% from 2.5%. The underlying inflation picture was benign.

(Regular Market Demystifier readers will recognise this dynamic — headline numbers screaming while the underlying data tells a completely different story. Textbook.)

And then, an hour and a half later, the University of Michigan dropped its preliminary April consumer sentiment reading...

...and it was ugly.

Sentiment crashed to 47.6 — an all-time record low for the series. One-year inflation expectations surged from 3.8% to 4.8%. American consumers are feeling the squeeze — oil prices, tariff uncertainty, and war anxiety all landing at once.

(The stagflation crowd had a field day with this one. Hot headline CPI + crashing sentiment + slowing GDP = textbook setup. Whether it materialises is another question entirely.)

The Rand barely flinched through all of it. After trading between R16.33 and R16.47 through the session, the pair settled back to close at R16.43/$, marginally weaker on the day but comfortably below R16.50.

The market's message: this inflation is transitory (yes, that word again), driven entirely by oil, and the ceasefire was already unwinding it.

For the week: a net move of roughly 55 cents in the Rand's favour. The strongest weekly performance of 2026.

Volatility and Risk Analysis

This was one of the most volatile weeks of 2026 for the Rand.

The numbers tell the story:

Open to Close Move: The week opened at R16.98/$ Monday morning and closed Friday afternoon at R16.43/$ — a 55c (3.2%) strengthening.

Average Daily Range: ~37c (0.22%)

Risk per $1 Million Exposure: R370,000

Maximum Single-Day Move: ~51c (3.0%) on Tuesday

Risk per $1 Million Exposure: R510,000

Weekly Range: 72c (R16.26 low to R16.99 high) — 4.3% swing

Risk per $1 Million Exposure: R720,000

For importers, this was a gift. Anyone converting dollars to Rand this week is paying roughly R550,000 less per million dollars than they were on Monday. But that gift came with a catch: the speed of the move meant that anyone who hesitated — even by a day — saw significantly different rates.

For exporters, the opposite applies. Dollar earnings converted to Rand this week are worth R550,000 less per million. The tariff pause is good news for export access...

...but the stronger Rand erodes the value of whatever you're exporting.

On the forecast front: Monday's short-term outlook had the target zone at R16.50–R16.13. Wednesday's low of R16.26 landed squarely inside that zone — the market hit the target and pushed well into it.

The cycle timing aligned perfectly with the geopolitical catalysts. The forecast had the direction right. The market delivered even more aggressively than the ideal path suggested...

...which is exactly what tends to happen when cycles and catalysts align.

The Week Ahead (13-17 April 2026)

SA: No major data releases scheduled. Watch for SARB commentary on inflation outlook post-US CPI, fuel price trajectory, and any tariff negotiation developments with Washington.

US: March PPI (Monday 14 April), Retail Sales later in the week. Fed speakers throughout. Kevin Warsh Fed Chair confirmation hearing — originally pencilled for 16 April — has been delayed; the Senate Banking Committee is awaiting paperwork.

Global: US-Iran negotiations broke down in Islamabad over the weekend — the two-week ceasefire window is still technically running (closes ~22 April), but with talks collapsed, the path to a comprehensive agreement just narrowed dramatically. Watch Hormuz shipping status and oil closely. China Q1 GDP mid-week — first reading on how 125% tariffs are affecting the world's second-largest economy. G20 Finance Ministers meeting in Washington DC. ECB and BoE rate decisions both at month-end — ECB facing oil-driven inflation pressure.

What to Watch:

The big question next week isn't about data — it's about durability.

Does the ceasefire hold? Oil below $100 hinges on Hormuz staying open. If the IRGC shuts shipping again, the war premium comes roaring back.

Does the tariff pause lead to deals? Trump has 90 days. Markets are pricing in negotiations, but there's no guarantee. For SA, the difference between 10% and 30% is existential for some exporters.

And the Rand? Our forecasts have the direction pointing lower still (Rand strength), with targets around R16.00. But after a 55-cent move in four days, some consolidation wouldn't be unusual...

...before the next leg takes hold.

"No forex strategy eliminates risk... but ignoring cycles guarantees losses. Markets move in waves... your hedging should too."

To your success~ James Paynter

P.S. This week was a powerful validation of cycle-based forecasting. Our short-term outlook called for the R16.50–R16.13 zone — the market delivered R16.26, landing well inside it. The direction was right. The timing was right. The target was hit.

If you're managing ongoing Rand exposure and wondering whether there's a better way than guessing...

...there is. In fact, we have done a full track record scoring of our forecasts since 2005 — yes, a full 20+ years of over 9,705 forecasts — and you can see the results here.

Want the full Rand cycle picture?

Register Free for Rand Forecasts