The Week the Rand Should Have Weakened...

...and Didn't.

Published 22 May 2026

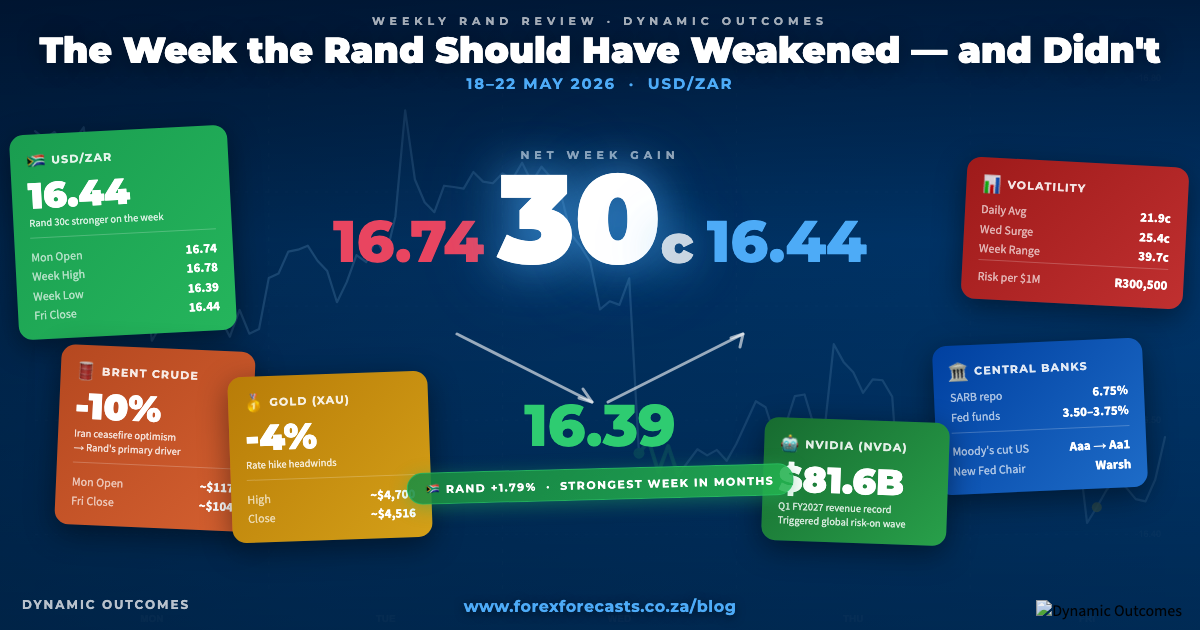

The Rand came into this week at R16.74/$. Last week had given back some of the prior fortnight's gains — a routine 22-cent softening on the back of US inflation data and a hawkish Federal Reserve.

This week, it gave it all back — and then some.

Thirty cents of Rand strength in five trading days. Not because South Africa delivered good news. Not because the SARB made a surprise move. Because oil fell 10%, the dollar was weighed down by a Moody's downgrade overhang, and NVIDIA reported a record quarter that sent risk appetite surging globally.

That is the week. Here's how it unfolded.

Key Moments — May 18–22, 2026

- Moody's stripped the US of its last AAA rating on May 16 (downgraded to Aa1), adding structural pressure on the dollar heading into the week.

- SA CPI landed at 4.0% on Wednesday — its highest since August 2024, driven by fuel costs. The Rand surged 25 cents anyway.

- FOMC Minutes revealed an 8-4 split — the most divided Fed vote in three decades. "Many" members favoured removing the easing bias entirely.

- Brent crude fell approximately 10% over the week on Iran ceasefire optimism, reducing US inflation expectations and dollar rate support.

- Kevin Warsh was sworn in as the 17th Federal Reserve Chair on Friday. His first formal FOMC: June 16–17.

- UMich Consumer Sentiment hit a final May reading of 44.8 — a new all-time record low, surpassing even the June 2022 inflation-peak trough.

Monday: A Tentative Start — and a Change in Direction 📉

The week opened with a piece of background noise that most market participants were still processing: Moody's had downgraded the United States on Friday the 16th.

Not a minor revision. Moody's was the last of the three major rating agencies to act — S&P and Fitch had already lowered the US decades ago. This final downgrade, from Aaa to Aa1, was pinned on fiscal trajectory: US debt on course to hit 134% of GDP by 2035. For the dollar, it was one more weight on the scale — a signal that the world's reserve currency issuer is not immune to the pressures that have historically destabilised smaller economies.

Against that backdrop, the Rand found early footing. Oil was moving, too. Iran ceasefire talks had gained intensity — reports of a possible 60-day extension to the existing truce and active discussions around de-mining the Strait of Hormuz. Lower oil prices mean lower US inflation expectations, fewer rate hikes priced in, a structurally weaker dollar.

That sequence matters for the Rand. When the dollar loses rate support, rand-denominated assets become relatively more attractive.

The Rand opened at R16.74/$ and drifted lower through Monday's session, closing at R16.61/$...

...A twelve-cent Rand gain before a single South African data point had been released.

Monday closed at R16.61/$. Tuesday would test whether the move was real.

Tuesday: A Pause Before the Data 📈

Tuesday was the counter-move.

The dollar steadied. Iran news turned ambiguous — reports emerged that Iran's supreme leader had drawn a harder line on uranium enrichment, complicating the ceasefire framework. Oil ticked back up. The Rand drifted from R16.65 at the open to R16.69 at the close. A four-cent setback.

In isolation, it barely registers. But context matters: the market knew that South Africa's April inflation figure was coming Wednesday morning.

April had been a difficult month for prices. The petrol price hike driven by Brent's surge above $120 during the peak of the Hormuz blockade had pushed pump prices sharply higher. A significant inflation reading was expected. What it would do to the Rand was the question the week was building toward.

Four cents was nothing. Wednesday was coming.

Tuesday closed at R16.69/$. The market was holding its breath.

Wednesday: The Number That Should Have Hurt — and the Surge That Followed 📉

This is the day the week was decided.

At 10:00 SAST, Stats SA released South Africa's April Consumer Price Index. The figure: 4.0% year-on-year. Up sharply from 3.1% in March — the highest inflation reading since August 2024.

The driver was fuel. Transport costs surged — petrol up 15.2%, diesel up 35.4%. These are the direct pass-through effects of April's pump price spike. Food inflation eased to 2.9%, which offered some relief. But the headline was hard to ignore.

Here is what the conventional playbook says: higher domestic inflation creates uncertainty, raises questions about the SARB's rate path, and typically weighs on a currency. You will hear that argument on every financial channel.

But at the same time the CPI data landed, Brent crude was collapsing. Iran ceasefire talks had progressed to a point where markets were pricing a genuine de-escalation — a 60-day extension framework, active Hormuz de-mining discussions. In one session, Brent fell around $8 to approach $108. Oil that had been above $120 just weeks earlier was retreating fast.

And NVIDIA had reported earnings overnight. $81.6 billion in revenue — a record. The AI trade was back, global risk appetite surged, and emerging market currencies caught the wave.

The dollar lost ground against everything. USDZAR dropped from R16.71 at the open to R16.45 at the close.

That is a 25.4-cent Rand strengthening in a single session.

Oil. The risk-on wave. Moody's overhang on the dollar. That is what drove the move. Not 4.0% CPI.

This is exactly why watching global sentiment matters as much as anything happening in Pretoria or Johannesburg. The biggest Rand move of the week happened on the same day South Africa's domestic inflation hit its highest level since August 2024. The two had almost nothing to do with each other.

Wednesday closed at R16.45/$...

...The week's direction had been decided in a single session.

Thursday: The Fed Speaks and the Rand Steadies 📈

Thursday brought the reality check — and it came from Washington.

The Federal Reserve released the minutes from its April 28-29 meeting. The tone was hawkish. Eight Fed members voted to maintain rates; four dissented. Among those who stayed, many were reportedly inclined to remove the easing bias from the statement — the market's shorthand for: rate cuts are off the table, and hikes may be coming back. It was described as the most divided Fed vote since October 1992.

For the dollar, the minutes provided brief support. Hawkish Fed expectations reduce the argument for selling the dollar. Oil also bounced modestly as Iran's position hardened again — the supreme leader signalled that uranium enrichment would stay inside Iranian borders.

The 10-year Treasury yield edged up to 4.62%.

The Rand paused — a minor 0.9-cent pullback to R16.52. After a 25-cent surge the previous day, the market was catching its breath. The week's gains were intact; Thursday's retreat barely scratched the surface of what Wednesday had built.

The SARB meeting, scheduled for 28 May, now loomed larger than ever. After Wednesday's CPI release, a rate hike had moved from unlikely to genuinely possible.

Thursday closed at R16.52/$. One more day.

Friday: Warsh In, Rand Holds 📉

Friday delivered the final chapter.

At the White House, Kevin Warsh was sworn in as the 17th Federal Reserve Chair, by Supreme Court Justice Clarence Thomas. He inherits a Fed in its most divided state in three decades, an economy running above 3.5% inflation, and a bond market still absorbing the Moody's downgrade and the Hormuz shock. His first formal FOMC meeting is June 16-17. Every word he says between now and then will be studied carefully.

The University of Michigan released its final May Consumer Sentiment reading: 44.8. Lower than the preliminary 48.2 reported the prior week, and a new all-time record low — surpassing the June 2022 trough of 50.0. A third consecutive monthly decline, driven by tariff anxiety, inflation fatigue, and rising mortgage and credit costs.

The S&P 500, in a somewhat counterintuitive moment, recorded its eighth consecutive winning week — driven largely by the NVIDIA-led AI rally that had started mid-week.

The Rand held — a modest 3-cent gain to R16.44. The week's gains intact, despite the noise.

From Monday's open at R16.74/$ to Friday's close at R16.44/$...

...just over 30 cents of Rand strength in five trading days.

Volatility & Risk Analysis

Thirty cents in five trading days. The move was not linear — it arrived in a single session.

Open to Close: The week opened at R16.74/$ Monday morning and closed Friday afternoon at R16.44/$ — a 30.05c (+1.79%) strengthening.

Weekly Range: 39.72 cents (R16.39 low to R16.78 high) — a 2.4% swing from top to bottom. At R10,000 per cent per million dollars of USD exposure, that's R397,200 of value at risk over the week.

Maximum Single-Day Move: ~25.4c on Wednesday — risk per $1 million exposure: R254,000.

Average Daily Range: ~21.9c — risk per $1 million exposure: R219,000 per day.

For importers, buying USD at Friday's close (R16.44) rather than Monday's open (R16.74) saved R30,050 per $100,000 of exposure. For exporters, Monday's open offered the best USD sale rate of the week.

The week's direction was set in a single Wednesday session — and nobody who only watched the SA economic calendar saw it coming.

In Other News 🌍

Oil's Biggest Weekly Drop — and What It Means for the Rand 🛢️

Brent crude fell from approximately $117 on Monday to $104 by Friday close — a 10% weekly decline, one of the sharpest since the Hormuz crisis began escalating in early 2026.

The driver was Iran ceasefire deal optimism. Any progress toward reopening the Strait of Hormuz pushes oil lower, which reduces US inflation expectations, which prices out Fed rate hikes, which weakens the dollar.

That transmission chain is exactly what drove this week's 30-cent Rand gain. Oil is telling you more about the Rand right now than most South African domestic data points. Worth watching closely next week.

The Week Ahead

Two things to watch closely next week.

The SARB MPC meets on 28 May. After Wednesday's 4.0% CPI reading — the highest since August 2024 — a rate hike is now back on the table. The repo rate has been at 6.75% since November 2025. A 25-basis-point hike would take it to 7.00%. Higher domestic rates can support the Rand through carry trade dynamics, but they also slow an already-fragile economy. South Africa's Q1 2026 GDP came in at 2.0% — below consensus. The SARB will be navigating a narrow path.

Kevin Warsh's first communications as Fed Chair will set the tone for June. He inherits the April meeting's hawkish blueprint: an 8-4 divided vote, "many" members wanting to drop the easing bias, and 3.8% headline inflation. Any signal of a more aggressive stance — or any softening — will move the dollar. The June 16-17 FOMC is the first formal meeting, but expect the market to scrutinise every speech and interview before then.

The week's data made one thing clear: global sentiment is driving the Rand more than any domestic number. That is what the forecasts are designed to navigate.

Until next week — to your success~

James Paynter

Want the full Rand cycle picture?

Register Free for Rand Forecasts