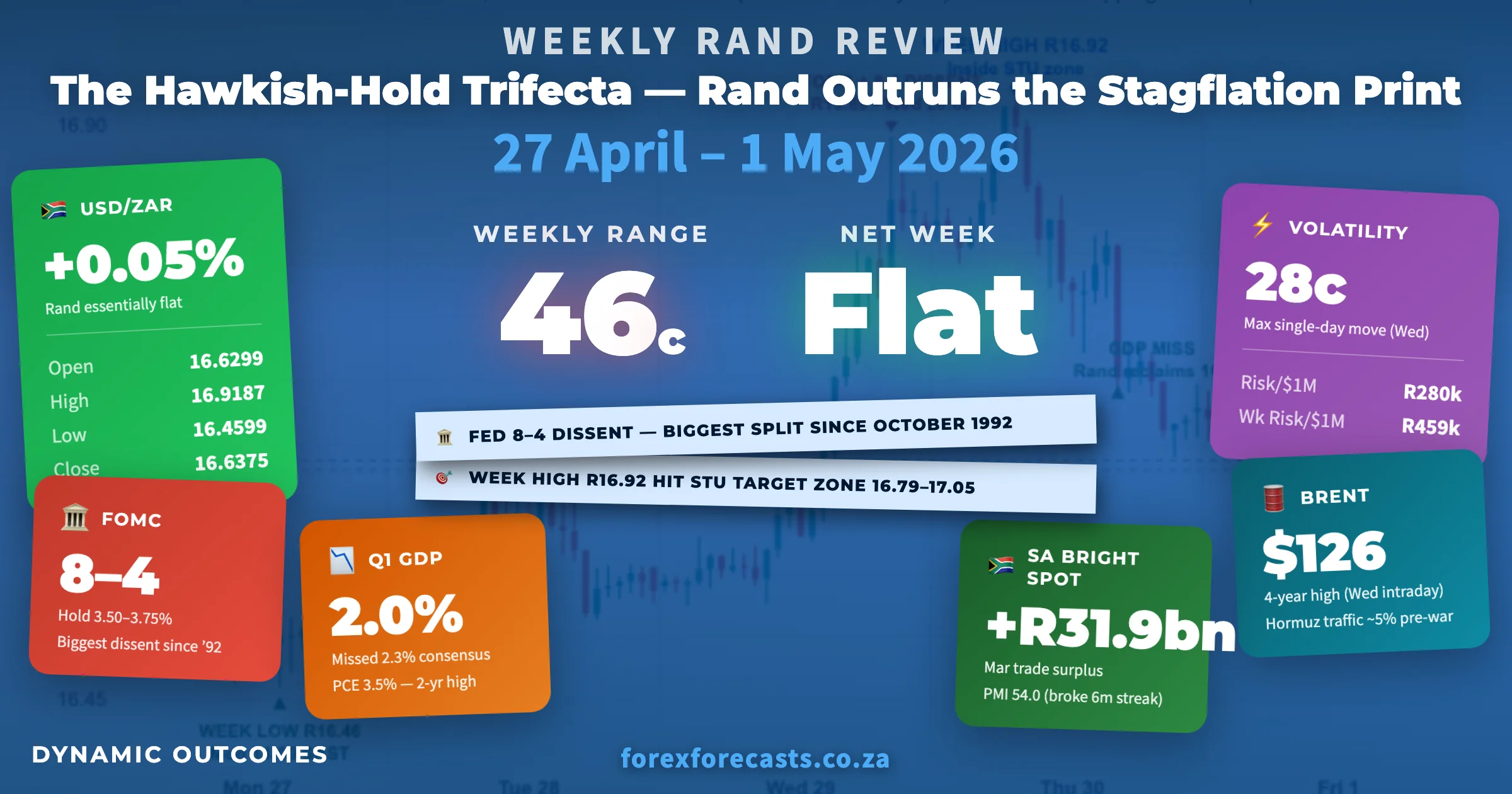

The Hawkish-Hold Trifecta Hit...

...And the Rand Finished Where It Started

Published 4 May 2026

Last week we said the Big Watch wasn't FOMC — it was GDP-versus-GDPNow on Thursday.

Both arrived... and both fired.

And the Rand?

It touched R16.92 on Thursday morning at exactly the level we'd flagged the Tuesday before, then walked back to R16.64 by Friday's close...

...essentially flat on the week, but the 46-cent range tells you it didn't get there quietly.

Here's how it played out...

But first — the call we put out Tuesday morning, before any of it happened. Topping zone, reversal trigger, invalidation level — all on the table:

Tuesday's STU outlook — topping zone R16.79–R17.05 flagged before the move.

KEY MOMENTS — 27 April – 1 May 2026 🔑

🏛️ FOMC Hold + 8–4 Dissent — Biggest Split Since 1992: Wednesday's decision held rates but split the Fed sharper than any meeting in 33 years.

🪑 Powell's Last Meeting as Chair: Senate Banking advanced Kevin Warsh 13–11 the same evening — Fed-chair handover risk now live for the week-of-11-May floor vote.

📉 Q1 GDP Missed at 2.0%: Consensus 2.3%, Atlanta Fed GDPNow 1.2% — composition softer than the headline.

🔥 Headline PCE 3.5% — Two-Year High: Same morning, the Fed's preferred inflation gauge accelerated to a two-year high. Stagflation flag, in print.

🛢️ Brent Touched $126 (4-Year High) Wednesday: Hormuz traffic ~5% of pre-war, US naval blockade actively enforced, Iran talks failed.

🇿🇦 SA Trade Balance +R31.9bn + Absa PMI 54.0: Rare double SA bright spot — PMI broke a six-month contraction streak with a single-month jump from 49.0.

🎯 Forecast Topping Zone Hit, Almost to the Cent: Tuesday's STU outlook called R16.79–R17.05; Thursday's high R16.92.

Monday: SA Closed, Quiet US Session, Week's Strongest Rand 📉

Monday opened at R16.63/$ — Freedom Day public holiday in South Africa, JSE and SA banks closed, US session running thin.

...and by 14:00 SAST the Rand had touched its strongest point of the entire week at R16.46. Just under twenty cents stronger than Friday's prior-week close.

Nothing on the US calendar of consequence (Fed already in blackout ahead of Wednesday's FOMC), nothing scheduled in Washington for the AGOA hearings until the following day. Just light positioning into the week's data deluge — which the market knew was coming.

Monday closed at R16.53/$ — essentially unchanged on the Friday-to-Monday gap, but the session low told you exactly how much room the Rand had to rally before the catalysts arrived.

Tuesday: AGOA Hearings Begin, FOMC Anticipation 📈

Tuesday opened at R16.53/$...

...and the session was a quiet one by the standards of what was coming.

The AGOA Section 301 hearings opened in Washington that afternoon, with South Africa among sixty economies in the dock under the forced-labour spotlight (manganese mining and Western Cape wine farms the named exhibits).

No verdict yet — those findings come later in the calendar — but the deeper context is the one we've been writing about for months: decades of policy choices by the SA government that assumed Washington wouldn't notice, eventually noticed.

The determination, when it lands, will significantly frame SA's future export outlook.

The Conference Board Consumer Confidence came in at 92.8 against an 89.0 consensus (the Iran-ceasefire window helped the survey period), and FOMC kicked off its two-day meeting — though the decision wouldn't land until Wednesday.

Tuesday closed at R16.54/$ — flat, with the session high R16.65 in the SA afternoon and the low R16.51 just before the New York close.

The market was waiting.

Wednesday: FOMC Hawkish Hold + 8–4 Dissent — Biggest Single-Day Move of the Week 📈

Wednesday opened at R16.55/$...

...and the day ran in two phases.

The first was an early-session push higher that took USDZAR from R16.55 at the SA open to R16.71 by 15:00 SAST — quiet drift up, oil pressing higher, dollar firm against most majors. Standard FOMC-eve positioning.

The second was the FOMC itself. The 20:00 SAST decision held the funds rate at 3.50–3.75% (which markets had priced) — but the dissent split was the story.

Eight members for the hold; four against. One dissenter wanted a 25-basis-point cut; three opposed keeping the easing-bias language in the statement. The last time the FOMC produced a four-vote dissent was October 1992.

Then Powell took the podium for his final press conference as Chair. He defended Fed independence against what he called Trump's "legal attacks", flagged Iran-driven energy uncertainty as the single biggest constraint on policy, and removed any meaningful easing bias from his own framing.

He also confirmed he'll stay on the Board past 15 May. Trump's response: "I don't care."

(Same evening, Senate Banking advanced Kevin Warsh 13–11 — the first fully partisan Fed-chair vote in modern history. Floor vote week of 11 May.)

The reaction across the next three hours was the cleanest hawkish-hold response we've seen in months — DXY pushed to 99.9 (a three-week high), and the S&P 500 closed at 7,209.01, the first close above 7,200 in history.

(April +10%, the best monthly performance since November 2020 — markets pricing the Fed's willingness to choose inflation control over growth support.)

And the Rand?

It sold off 28 cents in a single session — opening R16.55, closing R16.83, with the high struck at R16.89 at 20:00 SAST as the FOMC decision landed. The second-biggest single-session Rand move since the 8 April Iran shock.

(For exporters, the Wednesday-evening peak at R16.89 was the single best execution window before Thursday's data brought the dollar back to earth.

For importers, a one-session 28-cent selloff translates to R280,000 added to a $1 million conversion — though cycle-informed timing flagged the topping zone the prior afternoon, which is the value of having a map rather than a rearview mirror.)

Thursday: Q1 GDP Misses, PCE 2-Year High, Brent $126, Trade Balance Surplus, ECB & BoE Hold ⚖️

Thursday opened at R16.82/$...

...and within a six-hour window, the global calendar delivered four central-bank statements, three US data releases, and two SA readings. Then Brent touched its four-year high.

The week's high — R16.92 — was struck at 07:00 SAST in the early Asian session, before SA was even at its desks. After that, every direction was downward for USDZAR (and stronger for the Rand).

Stats SA released March PPI at 11:30 SAST — a modest pickup MoM, in line with the SARB tone shift the prior week.

The Bank of England held 3.75% at 13:00 SAST by an 8–1 vote, with one dissenter wanting a hike to 4.00%. Bailey's framing: "monetary policy cannot influence energy prices" — and if the Iran-war second-round effects materialise, that's "likely to warrant a forceful tightening."

SARS Trade Balance landed at 14:00 SAST with a +R31.9bn surplus (March, narrowed from R35.9bn in February but still robust). The ECB followed at 14:15 SAST, holding the deposit rate at 2.00% — and Lagarde explicitly confirmed the council had debated a hike, flagging the June meeting as "crucial."

Then 14:30 SAST. Q1 GDP missed at 2.0% q/q annualised — consensus had been 2.3%, with Atlanta Fed GDPNow at 1.2% (the GDPNow framing we flagged last week as the watch point).

Same release, Core PCE came in at 3.2% YoY — the highest since November 2023 — and Headline PCE 3.5%, a two-year high with the energy sub-component +11.6%. And as a counterpoint, Initial Jobless Claims at 189K, the lowest weekly reading since 1969.

(The composition is what mattered. The 2.0% headline was flattered by federal-employee snapback after the late-2025 shutdown, by Iran-related defence spending, and by import stockpiling ahead of the tariff window — real underlying growth was softer than the print suggested.

And inflation accelerating into a slowing economy is the dictionary definition of stagflation, which is exactly what Powell, Lagarde, and Bailey were all pricing the day before.)

Brent ran from $114 at the SA open to $126 intraday through the New York morning — a four-year high, with the US naval blockade now actively enforced and Hormuz traffic running at roughly 5% of pre-war average.

By the New York close it had settled back at $114, but the four-year-high print is what economists were citing in their Friday research notes.

The Rand reversed all day. The biggest hourly move of the week ran the other direction at 16:00 SAST — -10.4 cents as the Q1 GDP miss combined with the Trade Balance surplus to pull USDZAR sharply lower. By the New York close, the Rand had reclaimed sixteen cents from the morning high — closing R16.67/$ versus an open at R16.82.

And in other news...

The Hawkish-Hold Trifecta 🌍

Three central banks held this week, and all three came with hawkish dissents inside.

The Fed (8–4 split, biggest dissent in 33 years), the ECB (unanimous hold but with the council openly debating a hike), and the Bank of England (8–1 with one dissenter wanting a 25-basis-point hike). All three citing Iran-war energy as the binding constraint, and none of them anywhere near cutting.

The shorthand for the week is that monetary policy globally has stopped being about cuts.

Bailey's framing was the clearest — "monetary policy cannot influence energy prices" — and what it can do is anchor the inflation expectation while the supply shock works through. The cost of that anchoring is keeping rates higher for longer, which is what the curves are now pricing.

(The Rand benefits from this asymmetrically. SA carry remains intact while DM real rates rise, and the SARB's April Monetary Policy Review tone shift the prior week now looks like local pre-positioning for exactly this regime — the full implications take weeks to price in, and we'll be tracking it.)

SA's Quiet Bright Spot 🇿🇦

Two SA readings landed inside the noise.

First, the SARS Trade Balance March surplus at +R31.9bn — narrowed from R35.9bn in February, but well above forecast. Minerals, chemicals, vehicles drove the surplus despite imports rising 18.4% MoM.

Second, the Absa Manufacturing PMI for April came in at 54.0 — a striking jump from March's 49.0, breaking a six-month contraction streak. (PMI readings above 50 signal expansion; the move from 49 to 54 in a single month is the biggest one-month shift since 2021. Worth watching whether it holds for May.)

Combine these with Eskom's clean winter outlook (341 days without load shedding by week's end, briefed to Parliament Wednesday), and you have the most positive backdrop on SA fundamentals we've seen in twelve months.

Spot didn't price it dramatically — but the longer end of the SA yield curve absorbed it cleanly, and that's where capital flows get decided.

To get back to the Rand...

Friday: Workers' Day, ISM 52.7, Continued Rand Strength 📉

Friday opened at R16.68/$ — Workers' Day public holiday in South Africa, JSE closed, only US, UK and most of Asia trading.

...and the early-Asian push took USDZAR to R16.76 at 12:00 SAST before the tone shifted.

ISM Manufacturing for April came in at 52.7 — flat versus March, but the fourth consecutive expansion month and the eighteenth consecutive month of overall-economy expansion (New Orders 54.1, up 0.6 points; Production 53.4, down 1.7).

The data didn't alter the post-Q1-GDP-miss dynamic — the dollar stayed soft, and the Rand pushed to a day-low of R16.55 in the early NY afternoon, over twenty cents below the early-Asian high.

Friday's NY close arrived at R16.64/$ — the Rand giving back a few cents into the bell.

A 4-cent net Rand gain on Friday alone, which left the week essentially where it had started: Monday's open R16.63, Friday's close R16.64, with R16.92 touched and reversed in between.

(Worth noting: while the Rand was clawing back ground, the S&P 500 hit its second fresh all-time high in three sessions, with Brent at $111 and the VIX at 17.

A market that's been told stagflation is real, that the Fed is split eight-to-four, that an ally is at war — and is still pricing through the noise to print new highs. The risk-on regime we called intact last week is still intact this week.)

Volatility and Risk Analysis

This week's volatility was concentrated in a single session — Wednesday's 28-cent FOMC selloff drove most of it. Average daily range came in at 23.8 cents (28% wider than last week's 18.6c), and the 45.9-cent weekly range was 21% wider — both meaningful step-ups from last week, though still well short of what March delivered.

Open → Close: R16.6299 → R16.6375 — +0.75-cent (0.05%) Rand essentially unchanged

Risk per $1 Million Exposure: R7,500

Max Single-Day Move: 28.0 cents (1.69%) — Wednesday 29 April (FOMC Hawkish Hold day, R16.55 → R16.83 close)

Risk per $1 Million Exposure: R280,000

Weekly Range: 45.9 cents (2.78%) — R16.46 low (Mon 14:00 SAST) → R16.92 high (Thu 07:00 SAST)

Risk per $1 Million Exposure: R459,000

Average Daily Range: 23.8 cents (1.43%)

Risk per $1 Million Exposure: R238,000

For importers (those buying Dollars), Wednesday's 28-cent FOMC selloff was the pain point — R16.55 to R16.89 in eight trading hours is R340,000 added to a $1 million conversion. Thursday's reversal returned most of it, and Friday's close back at R16.64 left the week essentially unchanged on a Mon-open-vs-Fri-close basis.

(The cycle map flagged the topping zone the prior afternoon, between R16.79 and R17.05 — Thursday's R16.92 high sat almost dead-centre. The signal value is not in catching the high; it's in knowing the high was coming.)

For exporters (those selling Dollars), Wednesday's R16.89 was the cleanest execution window of the week — a single best price more than 30 cents above Monday's open. Anyone watching the FOMC tape and selling into the post-Powell spike captured the move; anyone holding through Thursday's data deluge gave most of it back.

📊 Our Track Record: Over 8,756 scored Rand forecasts since 2005 — 72.3% average accuracy, with 4 out of 5 forecasts in the right direction. See the full track record →

The Week Ahead — 4 May – 8 May 2026

SA: Calendar light Monday through Thursday — naamsa April vehicle sales early week, BER business confidence later. The bigger SA story is whether the Absa PMI surprise (49.0 → 54.0) holds in the S&P Global Whole Economy print on Tuesday.

US: April NFP releases Friday 8 May at 14:30 SAST — the report markets thought they were getting today. Add March JOLTS (Tuesday) and ISM Services (Tuesday) for the labour-market bookend after this week's 189K claims. Watch for the Senate floor vote on Warsh confirmation week-of-11 May (could land Friday 8 May or carry into the following week).

Global: Reserve Bank of Australia Tuesday (cut expected). Norges Bank Thursday. Iran/Hormuz status remains the meta-watch — Brent at $111 with the four-year-high $126 print fresh in everyone's mind.

What to Watch

The Big Watch is NFP on Friday. After this week's Initial Claims at a 57-year low and a Fed split 8–4 on the easing-bias language, the April payrolls print is the next inflection. A strong number entrenches "no cuts in 2026"; a weak number revives the pressure on a clearly divided FOMC.

The second is AGOA Section 301 follow-through. Hearings concluded; transcript pending; the USTR determination is the catalyst — likely weeks away. Worth watching for any leak-style reporting before the formal release.

The third is Iran. Hormuz traffic at 5% of pre-war, talks failed, Brent settled $111 with $126 fresh in memory. Any ceasefire resumption or escalation lands directly on the dollar through the inflation-expectations channel.

Two weeks ago we gave back fifteen cents on Iran. This week the heaviest macro tape of the year delivered a 46-cent range — and the Rand walked out essentially where it walked in.

Cycles, doing their work.

Until next week — stay sharp, stay skeptical, and don't let the headlines do your thinking for you.

To your success

James Paynter

P.S. The STU topping zone we flagged Tuesday landed dead centre — and reversed the same session. 8,756 forecasts, 72.3% accuracy. See the track record →

"Three central banks held this week.

All three debated hikes.

The cuts the world expected six months ago

are no longer on the table —

and the data is telling you why."

If you want to cut through the noise...

...and understand what's really moving markets

👉 Grab Your Free Copy of The Market Demystifier

Every issue cuts through the headlines to show you the forces actually driving the Rand, the Dollar, oil, and gold — so you can make smarter decisions on your forex exposure.

— James Paynter, Dynamic Outcomes

Want the full Rand cycle picture?

Register Free for Rand Forecasts