📈 One US jobs number just erased two weeks of Rand gains

Published 8 June 2026

For four days, the Rand looked comfortable.

It was holding the firm tone it had carried out of late May — backed by a fat trade surplus, a bumper month for new-car sales, and a central bank standing up in public to defend its inflation target...

...and then Friday afternoon, a single number out of Washington undid all of it.

The Rand closed the week 33 cents weaker.

Here's how it played out.

But first — the call we put out on 27 May, with the Rand still up at R16.67

USDZAR Short Term Outlook · 27 May 2026 · Direction: correcting, then down further · Target zone: 16.22–15.82 · Invalidation: above R16.77

That is the week we got. The Rand fell into the top of that target zone, touching R16.19 on Tuesday and holding the lows right through Thursday.

Key Moments (1–5 June 2026)

A few of the major headlines and events over the past five days:

🇺🇸 US Jobs Blew Past Every Forecast. Friday's payrolls landed far above consensus — and the Rand was in the wrong place when they hit.

💰 Gold Tumbles to a 2026 Low. South Africa's biggest export fell hard into Friday — and the Rand was never going to escape the fallout.

⚡ Petrol Hit an All-Time Record. From Wednesday the pump price set a new high — and the oil price had almost nothing to do with it.

🏛️ The SARB Doubled Down. Days after the hike, Governor Kganyago stood in front of a room of economists and told them precisely where he is taking inflation.

📉 Wall Street's Worst Day Since October. The US economy looked too strong on Friday — and that turned out to be exactly the problem for stocks.

Monday: A Busy, Firm Start 📈

Monday arrived buried under data, and the Rand took most of it in its stride.

The local calendar emptied its pockets before lunch: the Absa manufacturing PMI slipped to 50.8, the trade figures showed a R15.2 billion surplus for April, and new-vehicle sales came in at their best May since 2013. A mixed bag — a factory sector losing momentum, but an export engine and a car market both still running.

The Rand opened the week at R16.23/$ and probed lower through the morning, touching R16.19/$ — holding the strong zone it had carried out of late May — before the US session arrived.

Then, at 16:00 SAST, the first crack of what would become the week's real story: the US ISM manufacturing index landed at 54.0, its highest reading since 2022. The dollar found a little footing on it, and the Rand drifted back to close at R16.31/$. Six cents softer on the day, but still holding the firm range it had carried into June.

Tuesday: The Firm Zone Holds 📉

Tuesday was the week's quiet high-water mark.

The Rand opened at R16.34/$ and worked its way back down to R16.19/$ by midday — right back to its firm late-May lows — before settling at R16.24/$ into the close. Ten cents of Rand strength on the day, and a currency that genuinely looked like it had found something.

Two things gave it the air. Governor Kganyago stood up in front of a conference of economists and made the SARB's position unmistakable: last week's hike was deliberate, the 3% inflation target is the destination, and there would be no quiet retreat to the old comfort band. The other support came from across the Atlantic, where US job openings jumped to a near two-year high — strong, but not yet the kind of strong that frightens a currency market.

The Rand looked settled, and firm. It just didn't know it had two days left.

Wednesday: The Dollar Starts to Turn 📈

Wednesday was where the week began to tilt.

It opened at R16.24/$ and held its firm tone early before the afternoon turned against it. The pull came almost entirely from the US data: private payrolls beat at 122,000, and the ISM services index landed at 54.5 with its hottest price reading in nearly four years.

Hot American data does one thing to this market right now. It pushes the odds of a Federal Reserve rate cut further away — and pulls the odds of a hike closer. A dollar earning more carry is a dollar the Rand cannot easily fight. USDZAR climbed back to R16.36/$ by the close, eleven cents weaker on the day.

At home, the June fuel hike took effect, sending petrol to a record (more on that below) — but the price action was being written in Washington, not Pretoria. The S&P whole-economy PMI for South Africa had slipped to 49.6, into contraction for the first time in five months. The Rand barely noticed. It was watching the Fed.

Thursday: Coiling Before the Storm 📉

Thursday went almost nowhere, and that was the tell.

The Rand opened at R16.37/$, ground back to R16.22/$ at the intraday low, and closed at R16.31/$ — six cents firmer, in a session where almost nobody wanted to commit. US jobless claims ticked up to 225,000, but nobody was trading Thursday's data. They were squaring up for Friday's — a single release now twenty-four hours away: the May non-farm payrolls report.

A quiet day in a coiled market is rarely a quiet day. It is the held breath before the number.

Friday: One Number Erases the Week 📈

This is the session the week was always going to be decided in.

The Rand opened at R16.30/$ and held its ground through the morning, easing to R16.25/$ as the market waited for 14:30 SAST. Then the US Bureau of Labor Statistics released the May employment report, and the screen lit up.

The American economy added 172,000 jobs in May. The consensus had been for roughly 85,000 — the number came in at more than double. The unemployment rate held at 4.3%, and the two prior months were revised up by another 93,000 between them. There was no soft reading anywhere in it.

And the Rand?

It buckled — from R16.30/$ to R16.61/$ at the high, before settling at R16.56/$ into the New York close. Twenty-six cents of Rand weakness in a single afternoon — and with it, a fortnight of patient gains, wiped out. By the close, the Rand sat weaker than it had a full two weeks earlier.

The reaction was not contained to the Rand. The dollar surged to a two-month high, gold fell off a cliff, and US equities had their worst day since October — the nine-week winning streak snapped, the market's fear gauge spiking in an afternoon. A jobs report this hot rewrote the year's central question — not whether the Fed would cut, but whether it now has to hike — and every dollar-sensitive asset on the board repriced at once.

The Rand had done very little wrong this week. It simply found itself on the wrong side of the one number that mattered.

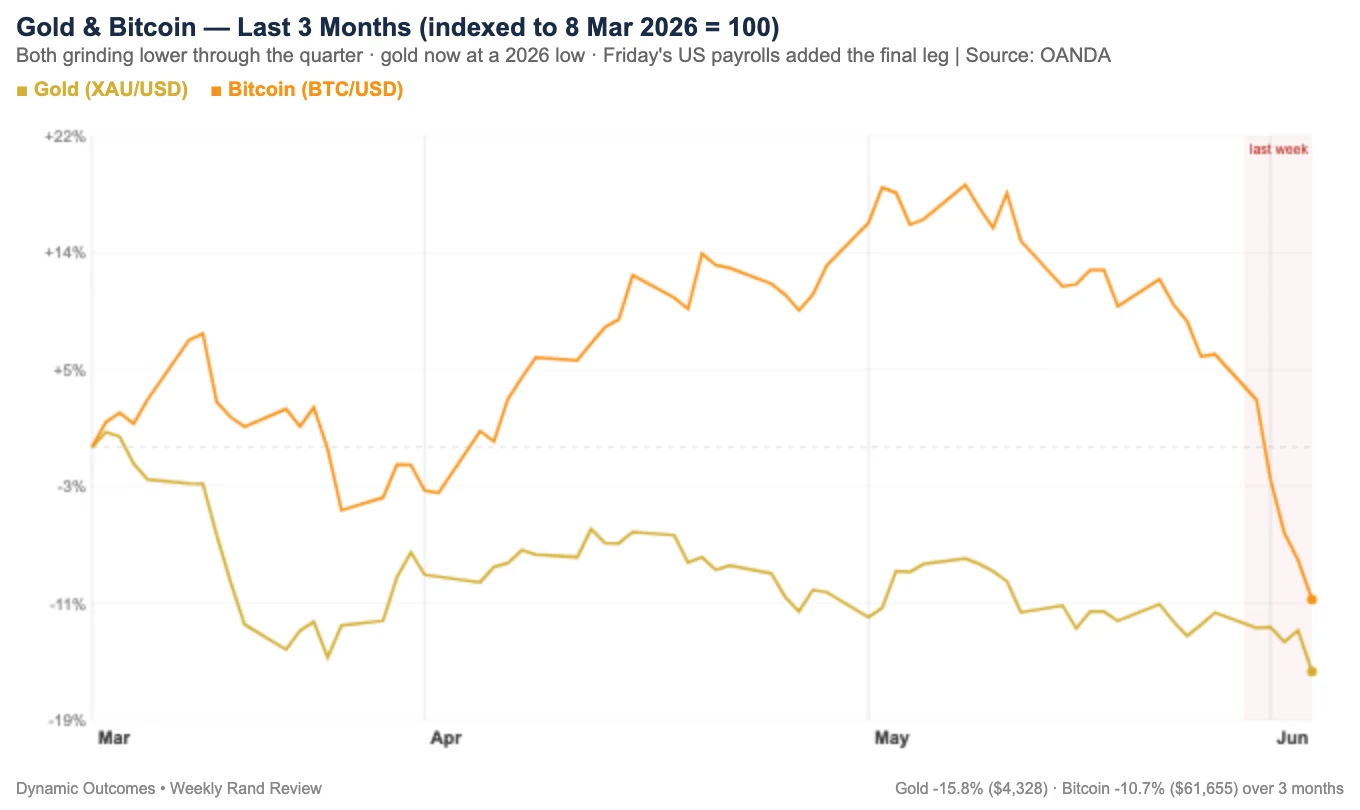

Gold Tumbles to a 2026 Low — and Why Your Rand Felt It 🥇

While the headlines went to the jobs number, the quieter story for South Africa was in the gold price. The metal fell to around $4,340 an ounce by Friday — a 2026 low — knocked down by the same strong-dollar wave that hit the Rand.

This matters because gold is South Africa's single largest export. When the gold price falls, the country's terms of trade soften, the export receipts that support the currency thin out, and the Rand loses one of its structural anchors. Friday's move was a double hit — a stronger dollar on one side, a weaker gold price on the other — and the Rand caught both.

Zooming out — gold and Bitcoin over the last three months, both grinding lower (gold to a 2026 low), with Friday's payrolls the final leg.

Petrol Hits a Record — and Oil Is Not the Reason ⛽

From Wednesday, the petrol price climbed to a fresh all-time high at the pumps — inland 95 unleaded crossing R28 a litre for the first time. The instinct is to blame the global oil price, but that is not what happened here.

The increase came almost entirely from Pretoria, not from crude. The Treasury reversed part of the fuel-levy relief that had been cushioning prices, and a higher slate levy was layered on top — together adding roughly R1.43 a litre to petrol. Diesel users, oddly, got relief. It is a tax story dressed as an oil story, and it lands on the consumer all the same.

Volatility and Risk Analysis

Thirty-three cents of Rand weakness in five trading days — and almost none of it was spread evenly. Four days of calm in a tight range, and then a single Friday afternoon that did roughly eighty percent of the damage.

- Open to Close: R16.23 (Mon) → R16.56 (Fri) — 33 cents of Rand weakening (2.0%). R330,000 of value swung per $1 million of exposure.

- Average Daily Range: 20.2 cents — R202,000 per $1 million per day.

- Maximum Single-Day Move: Friday's 36-cent range (R16.25 to R16.61) — R360,000 per $1 million, more risk than any other single session of the week.

- Weekly Range: 42 cents (R16.19 to R16.61) — a 2.6% swing, R420,000 per $1 million.

To put it in practical terms: an exporter who sold $100,000 at Friday's R16.56 close rather than Monday's R16.23 open banked roughly R33,000 more. For an importer, the maths ran the other way. The lesson sits in the timing, not the direction — the entire week's edge was decided in the four hours after 14:30 on Friday.

The Week Ahead (8–12 June 2026)

At home, Tuesday brings Q1 GDP — the single most important domestic number of the month, read alongside Kganyago's renewed 3% commitment. On the US side, the focus shifts to May CPI mid-week; after Friday's payrolls shock, a hot reading would all but cement the market's new flirtation with a Fed hike. Beyond it sits the main event: Kevin Warsh chairs his first FOMC meeting on 16–17 June. Globally, the ECB decides on 11 June (a 25bp hike near-fully priced), with the BoE to follow on 18 June.

The level that matters is R16.77 — the line our 27 May call drew. Hold below it and the lower targets stay live; break above and the down-view is finally off.

Weeks like this one are the whole argument for timing. The Rand can hand an exporter 33 cents — or take it from an importer — in a single afternoon, and the only thing that changes the outcome is knowing which window you're in before the payment lands, not after.

That is exactly what Strategic Rand is built for — cycle-based USD/ZAR forecasting for South African importers and exporters, with the levels, the targets, and the invalidation lines mapped out before the week begins.

To your success

James Paynter

Want the full Rand cycle picture?

Register Free for Rand Forecasts