📉 One US Jobs Number Cracked the Dollar — and the Rand Took Back 21 Cents

Published 6 July 2026

For three weeks the story has been Washington's, and Washington has been winning.

A new Fed chair drew a hawkish line in mid-June, the dollar climbed to a thirteen-month high, and the Rand spent a fortnight on the back foot for reasons that had nothing to do with South Africa.

This week, the line started to bend. One jobs number — released a day early for the holiday — did the bending.

And the Rand? It took back twenty-one cents.

Here's how it played out.

Key Moments (29 June – 3 July 2026)

A few of the major headlines and events over the past five days:

🇺🇸 The US Jobs Report Landed a Day Early. Thursday's number was meant for Friday — and what it revealed took the dollar's month-long run apart in an afternoon.

💰 The Dollar Came Off the Boil. Fresh off a thirteen-month high, the greenback gave ground all week as the case for another rate hike quietly thinned.

⛽ South African Drivers Caught a Break. The 1 July fuel adjustment brought real relief at the pump — even as the lights bill went the other way.

📊 Gold Turned With the Dollar. The metal broke a four-week slide with its first weekly gain — a clear sign the dollar's run was rolling over.

Monday: A Cautious, Firm Open 📉

The Rand opened the week at its softest, starting at R16.46/$ and briefly touching R16.50/$ in the first hour — the weakest point it would see for the next five days.

From there it steadied. There was no local data to trade and a US calendar that was front-loaded and holiday-shortened, so the session became a waiting game — desks squaring up ahead of a jobs report that everyone knew had been pulled forward to Thursday.

The dollar, for once, was not pressing. Having spent the prior fortnight climbing, it opened the week a fraction off its highs, and the Rand quietly used the breathing room. (A high-yield currency asks for very little — just for the dollar to stop leaning on it.)

It closed at R16.42/$, almost four cents firmer on the day — a small gain, but the first sign that the wind had shifted.

Tuesday: The Grind Lower 📉

Tuesday extended Monday's tone without ever raising its voice.

The Rand opened at R16.45/$ and spent the session drifting the right way, reaching R16.39/$ by the close — a steady, all-day firming with no single catalyst behind it, just a dollar that had stopped going up.

Across the Atlantic, the one genuinely hot number of the week arrived: US job openings jumped to a two-year high of 7.6 million, comfortably ahead of forecast. On another week that would have handed the dollar fresh fuel...

...but the greenback barely flinched, and the Rand read the silence correctly.

At home, month-end brought the trade figures, and they were softer — a small R1.8 billion deficit for May after April's surplus. It moved nothing. The Rand closed two-and-a-half cents firmer, its eyes already on Thursday.

Wednesday: A Full In-Tray at Home 📈

Wednesday was the week's busiest day for news and its quietest for the Rand — which tells you something about where the real driver sat.

The local diary was packed. The 1 July fuel adjustment landed a hefty cut at the pump; a fresh round of electricity tariffs went the other way; the Absa manufacturing gauge slipped back into contraction while new-vehicle sales came in strong. (More on all of it below — but none of it, on the day, moved the currency.)

The bigger tell came from the US. Private payrolls undershot at just ninety-eight thousand, and a closely watched factory survey missed as well...

...the first small crack in the dollar's story, a day before the big one.

The Rand opened at R16.39/$ and closed at R16.41/$, a couple of cents softer — the week's only down day, and a coiled one. Everyone was waiting for the same thing.

In Other News 🌍

The Dollar's Turn 💰

Step back from the single afternoon and the week tells a bigger story: the dollar's June run is unwinding.

For most of last month the greenback had one thing going for it — the belief that a hawkish new Fed chair might actually raise rates again, when the rest of the developed world is done tightening. That belief drove it to a thirteen-month high and cost the Rand thirty-one cents in a fortnight.

This week chipped away at it. A soft jobs report, a weak private-payrolls number, and a collapse in the prices businesses are paying all pointed the same way — the case for another hike is thinning. Even the Fed chair, speaking in Europe on Tuesday, conceded that inflation expectations had "eased over the past month," while still insisting prices were too high.

The proof showed up across the board. The dollar index slipped back below 101, gold posted its first weekly gain in over a month, and Wall Street's Dow closed at a record before shutting early for the holiday — all of it the same trade, running in reverse.

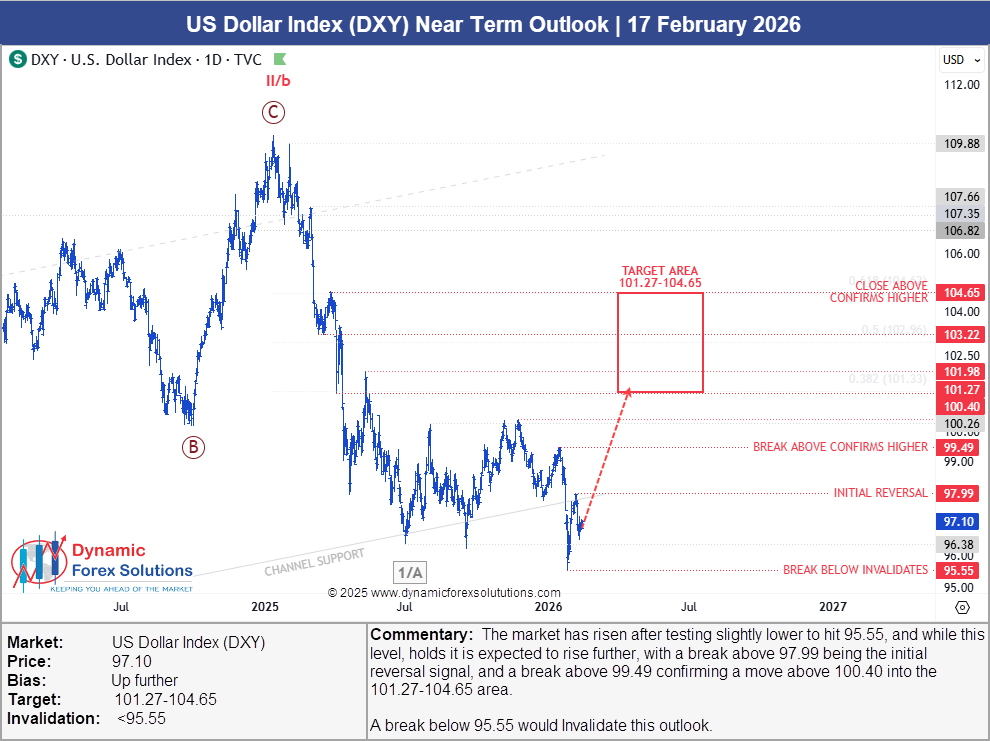

And for regular readers, none of it came as a surprise. Back in February we put out a dollar-index call — up from 97 into a 101.27–104.65 target zone, with the level that would prove it wrong marked below. The dollar spent the next four months climbing into it, tagged the top of the zone at a thirteen-month high a fortnight ago, and turned this week — almost exactly where the chart said it would.

US Dollar Index Near-Term Outlook, issued 17 February 2026 — a call for the dollar to rise into 101.27–104.65. It spent the following months doing exactly that.

That is the same cycle-based read we publish on the dollar, gold, the euro and Bitcoin — the global forecasts that sit alongside our Rand work. If you want the map before the market moves, see them at The Market Demystifier.

South Africa's Cheaper Tank 🇿🇦

Beneath the dollar's noise, the home front handed households a genuine win.

The 1 July fuel adjustment brought real relief — around two rand off a litre of petrol and more than three off diesel — the direct result of the oil price sliding through June and a Rand that has refused to fall apart.

For an economy where the fuel bill feeds into almost everything, that is real disinflation arriving right when the Reserve Bank wants to see it. (Though the taxman gave a little back the same day, with a fresh round of electricity tariffs adding around nine percent to the municipal bill.)

The rest of the local ledger was a study in two halves. Manufacturing slipped back into contraction, business confidence sank to its lowest in years, and yet the services side edged into growth and new-vehicle sales notched a twenty-first straight month of gains — the strongest June in nearly two decades.

And yet the Reserve Bank is not relaxing. The Governor used the week to remind everyone that inflation expectations have crept above target, and that another rate move is firmly on the table when the committee meets on 23 July. A cheaper tank is welcome; it does not, on its own, change the Bank's mind.

USD/ZAR hourly, 29 June – 3 July 2026 (SA time) · four quiet sessions and one sharp Thursday break on the US jobs report, from R16.46 to R16.24 (OANDA)

To get back to the Rand...

...because for all the news at home, the week's real turn was still to come — and it came from a single American number.

Thursday: The Number That Turned It 📉

Thursday was the session the week had been building toward, and it arrived at half-past two.

Through the SA morning the Rand had done nothing, holding a tight band around R16.39/$ with the market unwilling to commit before the data. Then, at 14:30 SAST — a day earlier than usual, cleared out of the way of Friday's holiday — the US June jobs report hit the screens.

It was soft — badly soft. The economy had added just fifty-seven thousand jobs against expectations of well over a hundred thousand, and the two prior months were revised down by a combined seventy-four thousand. The labour market the Fed had turned hawkish to cool was, it turned out, already cooling on its own.

And the Rand? It strengthened.

The dollar sank on the number, its two-year yield falling and the bets on a September rate hike halving within minutes, and the Rand tore through R16.30/$ to touch R16.22/$ — a fifteen-cent swing inside a single afternoon.

There was a catch buried in the report, and it is worth seeing. The unemployment rate actually fell, to 4.2% — which reads like strength until you notice why.

It fell because people stopped looking for work, with the share of Americans in the labour force dropping to its lowest since early 2021...

...and a shrinking workforce is not a healthy one. (The headline flattered; the detail did not — and the market traded the detail.)

The Rand closed at R16.25/$, a full fifteen-and-a-half cents firmer than Wednesday — the day that made the week.

Friday: Holding, With Wall Street Dark 📉

Friday's job was to keep Thursday's gains, and — with the US closed for Independence Day — it had a thin, quiet stage on which to do it.

The Rand opened at R16.26/$ and drifted lower still through a sleepy session, touching R16.19/$ — its strongest point of the entire week — before settling.

There was little to push against. Wall Street was dark, the local desks wound down into the weekend, and the only real market tell was gold, which capped a 2% weekly gain that told the same dollar-down story from a different angle.

By the close it stood at R16.24/$, holding almost all of Thursday's move — and a full twenty-one cents firmer than where Monday had begun.

Volatility & Risk Analysis

Twenty-one cents. That was the Rand's net gain across the week — but nearly three-quarters of it arrived in a single Thursday afternoon.

Open to Close: The week opened Monday at R16.46/$ and closed Friday at R16.24/$ — 21 cents of Rand strength (1.28%), or about R211,000 per $1 million of exposure.

Weekly Range: just over 31 cents (R16.19 low to R16.50 high) — a 1.9% swing top to bottom, or R313,000 per $1 million.

Maximum Single-Day Move: Thursday's 20-cent range — R202,000 per $1 million in one session, almost all of it in the hour after the jobs report.

Average Daily Range: just under 13 cents — R128,000 per $1 million per day, another quiet week by that measure, with Thursday doing nearly all of the work.

A note on the crosses, because it matters for what drove the week: the Rand gained most against the dollar, less against the euro, and only marginally against the pound. When a currency firms hardest against one counterpart and barely against the others, the story is about that counterpart — and this was a dollar story, not a Rand one.

To put the timing in practical terms: an importer who waited and bought dollars into Friday's R16.24 rather than Monday's R16.46 saved roughly R21,000 per $100,000 — while an exporter who sold early, into Monday's open rather than Friday's close, gave up about the same. The edge, as ever, sat in reading the direction before the afternoon that delivered it.

The Week Ahead

The holiday-shortened week gives way to a fuller one, and the balance of risk tilts back toward events that could interrupt the Rand's run.

At home, the focus turns to the Reserve Bank. There is no decision until 23 July, but with the Governor openly flagging a possible further hike and inflation expectations drifting up, every SARB comment between now and then will be parsed for intent. Watch, too, for whether the cheaper fuel starts to show up in the forward inflation picture.

On the US side, the calendar reopens after the holiday with the services survey and the minutes of the Fed's last meeting — the first detailed look at how divided the committee really is under its new chair. After a jobs report that undercut the hawkish case, any hint that the Fed is softening its tone would keep the dollar on the back foot.

Globally, two things sit on the near horizon: a decision from the oil producers on whether to add more barrels from August, and a US trade hearing that could put fresh tariffs on South African goods. Either could shift the mood quickly.

Until next week — to your success~

James Paynter

This was a week that made a simple point: the Rand's biggest moves are still being decided in Washington, not Pretoria. South Africa cut the price of fuel and sold more cars — and none of it mattered as much as fifty-seven thousand American jobs that failed to show up. That kind of read — knowing where a currency is structurally headed, and the lines that tell you the moment it turns — is what 21 years and over 8,750 scored Rand forecasts at 72.3% average accuracy are built on.

See the latest USD/ZAR forecasts at Strategic Rand.

Want the full Rand cycle picture?

Register Free for Rand Forecasts